The Add Allowances window lets you add and edit the allowances to be used when setting up your Employees. MYOB Exo Payroll comes with several default allowances that you can edit to make them appropriate to your specific situation, as well as creating new ones. You can also globally load allowances to all employees. Select Step Two from the Payroll Setup Cycle and the following window appears:

The Maintenance menu, which also provides access to Allowance maintenance, can also be chosen at any time by pressing F2.

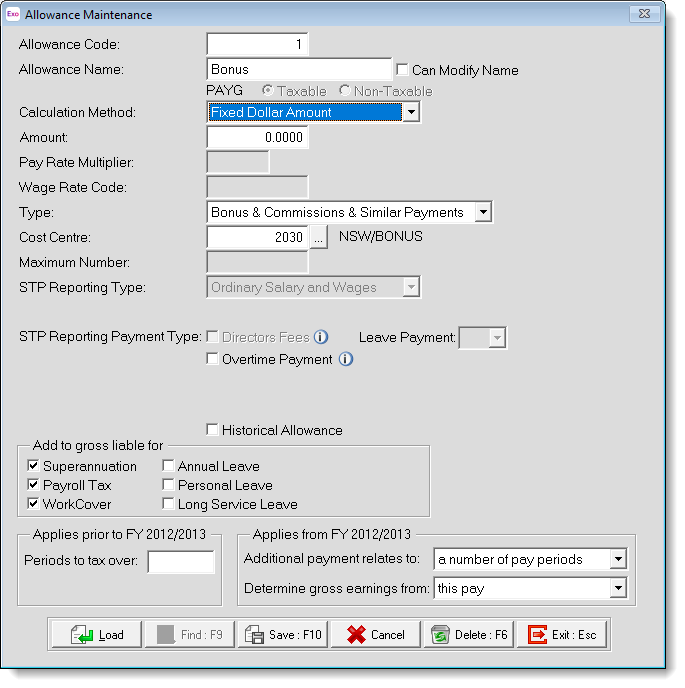

When you first enter the Allowance Maintenance window, all the fields are blank with the exception of the Allowance Code field. This allows you to either enter the code for a new allowance or enter the code of an existing allowance to edit it. You can also click Find or press F9 to select an existing allowance from a list.

Allowance Code Enter the code number you want to list this allowance as. This number can be up to 3 digits in length (1-999).

Allowance Name Enter the name of this allowance (up to 20 characters).

Can Modify Name Switching this option on gives you the ability to modify the name of an allowance for a particular employee. This means that when the allowance is paid to an employee, you are able to edit the allowance's name. The allowance will still be tracked and costed to the allowance number.

PAYG Select whether or not this new allowance is to be taxable by selecting either the "Taxable" or the "Non-Taxable" option. These options become disabled once transactions exist for the allowance.

Calculation Method Your allowances can be calculated using a number of methods. Choose from:

-

Fixed Dollar Amount - This means that the allowance is to be a fixed sum, such as a Clothing Allowance of $30.00 per week. If the amount is to be a varying amount depending on the employee, then choose this calculation type but do not enter in any amount in the next field e.g. a fixed dollar amount bonus allowance that is different for each employee and will be entered when running the pay.

-

% of Salary and Wage - This means that the allowance will be calculated as a percentage of the total gross wage or salary that is being paid to an employee. e.g. an employee has a salary of $500.00 gross and the allowance is set to pay 5%, then it will automatically pay $25.00.

-

Total Hours - This means that you set the rate to pay an employee and it will automatically calculate the allowance based on the total number of hours worked. e.g. an employee works 40 hours normal time and 5 hours overtime and his allowance is for tool money at .10c per hour then this will pay 45 hours x .10c.

-

Equivalent Hours - This type is very similar to Total Hours but instead it uses the hours based on the pay rate used. For example, as above a tool money allowance is .10c per hour for a 40 normal hours, 5 overtime (time and a half) hours, then it will pay 47.5 hours x .10c, as 5 x 1.5 = 7.5.

-

Specific Hours - This means that you enter the number of hours to pay this allowance.

-

Rated Units - This means that you have either a payment or an item that is valued at a certain rate per time it is paid. When this allowance is paid, enter the number of units to pay, e.g. to set a plant cutting at 10c per plant then select this calculation method and set the rate at .10.

-

Hourly Rate - This calculation type will use the hourly rate for an employee and pay the number of hours that you enter in for that pay period. This is the calculation method you would choose for Bereavement Leave etc. Remember when paying an allowance using this method that you need to enter in the pay rate type to be used, e.g. 1 for ordinary hourly rate, 2 for 1.5x the hourly rate.

-

% of Total Gross - This method is a non-taxable method only. This will calculate an amount based on the total gross pay of the employee.

-

Motor Vehicle - The motor vehicle/mileage method of calculating the allowance amount is the same as the Rated Units method; however the liability for Payroll tax is treated differently. For example, if in your state, the first 50c of a mileage allowance is not liable for payroll tax, set up the allowance as follows:

(Motor Vehicle) Rate: 00.75c

(Motor Vehicle) Rate Exempt from Payroll Tax: 00.535c

In effect this means that only 21.5c in the dollar will be subject to Payroll tax, rather than the full 75c per km. -

Accommodation - Operates similarly to the Motor Vehicle method. The method of calculating the allowance amount is the same as the Rated Units method; however the liability for Payroll tax is treated differently. For example, if in your state, the first $130 of one night's accommodation allowance is not liable for Payroll tax, set up the allowance as follows:

(Accommodation) Rate: $200.00

(Accommodation) Rate Exempt from Payroll Tax: 130.00

In effect this means that only $70 will be subject to Payroll tax, rather than the full $200 per night.

Amount/Rate/Percentage Enter the amount or rate that the allowance you are creating is to use. Remember if the amounts or rates vary from employee to employee then leave this field blank and enter the particular amount or rate for the employee in their specific Standard Pay/Allowances window.

Pay Rate Multiplier If you are using the "% of Wage and Salary", "Total Hours", "Equivalent Hours" or "Hourly Rate" calculation methods, this field is used to determine the pay rate multiplier to use.

Wage Rate Code If you are using the "% of Wage and Salary" or "Hourly Rate" calculation methods and you have multiple hourly rates enabled, you are able to specify which wage rate code this allowance will use in its calculations. If you do not enter anything into this field when it is accessible Exo Payroll will calculate using the default of wage rate code 1.

Type Select the type of allowance. Choose from:

-

Normal - This is the default used for most Allowances.

-

Reimbursement - This is only to be used for non-taxable reimbursements where you are paying back an employee for expenses they incurred on behalf of the business.

-

Withholding Payment - Select this option if you are using the Allowance to pay the GST component to Contractors.

-

Back payment & lump sum arrears - A back payment or lump sum arrears is a retrospective payment made to an employee, which is determined on the difference between what an employee was paid and the amount he or she should have been paid. Payments could be related if the employee was not paid in full for hours work or for overtime, and could also include the applying of a pay rise to previous periods.

-

Bonus & commissions & similar payments - A bonus is usually made to an employee in recognition of performance or services and may be calculated as a percentage of the proceeds from a particular business transaction. These payments may not necessarily be related to a particular period of work.

Commissions are typically payments made as recognition of performance or service, and may be calculated as a percentage of the proceeds from a particular transaction or series of transactions.

A payment will be treated as similar to a bonus if it is an amount of a one-off nature which does not relate to work performed in a particular period. Examples include a once only payment made to an employee as compensation for a changed work location, an amount paid as a sign-on bonus to a worker entering a workplace agreement or a one-off allowance.

If the bonuses or commissions are paid in respect of overtime (i.e., if they are wholly referable to overtime hours worked), ensure that you select the Overtime Payment checkbox. -

Other additional payments - These are one-off payments that are unlikely to occur again or do not specifically relate to a particular pay period.

-

Paid Parental Leave - This is for Allowances that are used to pay an employee Paid Parental Leave.

-

ETP - This type is only available for Non-Taxable Allowances. It is intended for Employment Termination Payments (ETPs), as it allows certain liabilities to be set.

The ATO specifies two calculation methods for calculating withholding on back payments, lump sum arrears, bonus and similar payments, commissions and other additional payments: Method A and Method B. MYOB Exo Payroll uses Method A, which calculates withholding by apportioning additional payments made in the current pay period over the number of pay periods in a year, and applying that average amount to the gross earnings in the current pay period.

Cost Centre The Cost Centre for each Allowance will automatically default to the employee's own default Cost Centre, which is the one you place against an employee when you add them to the Payroll. If you want to cost an allowance to a different Cost Centre, type in the Cost Centre number that you want this allowance to be costed to. Remember that this will override any employees' default Cost Centre.

Maximum Number To give better control over the payment of certain allowances, the Maximum Number feature sets the maximum number of times that the allowance is permitted to be paid in one entry. If you set this number, then any time you try to pay more than the allowed maximum an error box will appear. This means that if you set the maximum number for meal money to 7, you would not be able to pay more than seven meal moneys at one time.

STP Reporting Type Select the reporting category for this allowance:

-

Ordinary Salary and Wages - The Allowance will be included in employees' gross income amounts. Some payments belong in the Gross field, along with the normal wages and salary. They include Allowances to compensate for specific working conditions and payments for special qualifications or extended hours. For example, normal home to work transport expenses, annual leave or bonuses, amounts paid for unused long service leave, unused annual leave and other leave related payments that have accrued after 17 August 1993, except if the amount was paid because the payee ceased employment under an approved early retirement scheme, invalidity or bona fide redundancy (see notes on Lump Sum Payments below).

This does not include amounts that are shown separately as CDEP salary or wages, Allowances, Lump sum payments, return to work payments.

To completely exclude a payment from Single Touch Payroll reporting, set the Allowance to "Non-Taxable" and set the Allowance Type to "Non-Reportable". -

Allowance Item - Such as tool allowances and motor vehicle allowances, including car expense payments on a cents per kilometre basis. When this option is selected, amounts for the Allowance will not be included in gross income, but will be broken out into categories. Specify the category for this Allowance using the Single Touch Payroll Category field.

-

CDEP Payments - This is the amount of salary or wages you have paid to the payee from a Community Development Employment Project wages grant.

CDEP Payments are no longer supported.

-

Lump Sum Payment A - Unused long service leave that has accrued after 15 August 1978, but before the 18th of August 1993. Unused annual leave and other leave related payments that accrued before 18 August 1993. Unused long service leave, unused annual leave and other leave related payments that have accrued after 15 August 1978 if the amount was paid because the payee ceased employment under an approved early retirement scheme, because of invalidity or because of a bona fide redundancy.

-

Lump Sum Payment B - Amounts paid for unused long service leave that have accrued before 16 August 1978.

-

Lump Sum Payment D - The tax free component of a bona fide redundancy payment or an approved early retirement scheme payment.

-

Lump Sum Payment E - Amounts paid for back payment of salary and wages, which have accrued more than 12 months ago. Also, any return to work payments.

-

Non Reportable - Any amounts that are exempt income and/or foreign source salary and wage income. These amounts should not be included in the Gross payments.

-

Exempt Foreign Employment Income - The Allowance is Exempt Foreign Employment Income (EFEI), which is non-taxable, but is reported via Single Touch Payroll. Information on what sorts of foreign income are exempt is available at the ATO website.

-

Return to Work Payment - This should only be used for non-WHM employee payments.

STP Reporting Payment Type This section was added for STP Phase 2. It includes the following options:

-

Directors Fees Tick this checkbox if the Allowance relates to fees paid to the director of a company, or someone who performs the duties of the director of a company.

-

Overtime Payment Tick this checkbox if the Allowance relates to payment outside of an employee’s normal hours of work.

-

Leave Payment For Allowances that relate to the payment of leave, this dropdown lets you categorise the leave payment as one of:

-

Cash out of leave in service

All cash out of leave in service is for leave classified as ordinary time earnings. If there are other entitlements to leave that are ordinary time earnings, you must also report those cash-out payments as Leave Payment Type-C (Cash out of leave in service). However, if the cash out of leave in service is for leave whose absence is not ordinary time earnings, ensure that you select the Overtime Payment checkbox.

Another example of cash out of leave in service that is not ordinary time earnings is Time Off in Lieu (TOIL). TOIL is provided in some awards and registered agreements to allow an employee to take paid time off work instead of being paid overtime pay.

The absence may be granted at the overtime single time equivalent (STE) hours or actual worked hours.

The absence entitlement, if not taken within the specified time permitted under the industrial instrument, would be paid out as the original overtime penalty hours.

This type of cash out of "leave" is not ordinary time earnings, therefore ensure that you select the Overtime Payment checkbox. -

Unused leave on termination

-

Workers’ compensation

-

Ancillary and defence leave

-

Other paid leave

-

When using an allowance that relates to paying leave, any Leave Balances need to be manually adjusted accordingly.

Override Tax Rate A taxable allowance will automatically be added to an employee's gross pay and taxed as such. If you want this allowance to be taxed at a different tax rate, type in the tax rate (as a percentage) that you want this allowance to be taxed at.

For Allowances where the Type is set to "Bonus & commissions & similar payments", this field only applies to pays prior to the 2012 - 2013 financial year.

Rate Exempt for Payroll Tax When the Calculation Method is set to "Motor Vehicle" or "Accommodation", enter the amount of the allowance that is not subject to Payroll tax. (See the description of the Calculation Method property for setup examples.)

Historical Allowance Over a long period of time, you may find that some allowance codes are no longer required. To avoid having to scroll through long lists of unnecessary codes, you can hide obsolete codes from the code lookup screens by marking the codes as historical. You cannot mark an allowance as historical if it is currently included in employees' Standard or Current Pays. You may reverse the historical setting at any time, making the code current again.

There is an exception to the rule above: you can mark an allowance as historical if the only employees it is associated with are terminated employees; however if a terminated employee is reinstated, any historical records associated with them will be reactivated, i.e. the Historical Allowance option will become disabled.

Withholding Tax Rate When the Type is set to "Withholding Payment", enter the rate at which GST is calculated.

Include in Hours Paid When the Calculation Method is set to "Rated Units" or "Hourly Rate", selecting this option adds the allowance units to the total hours paid for the selected leave type(s). This has an effect on leave or RDO calculations.

Different states have different rules for whether or not leave accumulates during workers compensation (WorkCover) - see "Annual leave & sick leave during workers compensation" on the Fair Work website for details. If your organisation operates in multiple states with different rules around leave and workers compensation, you will need to set up a separate WorkCover allowance to use for each state, with the appropriate Include in Hours Paid options ticked.

Add to gross liable for

Certain Allowances have an effect on other payment items, e.g. shift allowances are liable for Superannuation, whereas reimbursements are not. The options in this section let you select which of the following pay items this Allowance is liable for:

-

Superannuation

-

Payroll Tax

-

WorkCover

-

Annual Leave

-

Personal Leave

-

Long Service Leave

When "ETP" is selected for the Type, only the Superannuation, Payroll Tax and WorkCover options are available.

Properties that apply prior to the 2012 - 2013 financial year

Periods to Tax Over When the Type is set to "Bonus & commissions & similar payments", enter the number of periods over which the bonus should be taxed. Because this value may differ every time you pay the bonus, this field should usually be left blank. This will allow you to change it when you pay the Bonus to the employee.

Properties that apply to the 2012 - 2013 financial year and later

The following properties are available when the Type is set to "Back payment and lump sum arrears", "Bonus & commissions & similar payments" or "Other additional payments". They apply only to pays in the 2012 - 2013 financial year and later.

Additional payment relates to Select whether this Allowance payment relates to a single pay period or a number of pay periods.

Determine gross earnings from This property is available when the Additional payment relates to property is set to "a number of pay periods". In this case, specify how the gross earnings should be calculated for taxation. Choose from:

-

this pay - gross earnings are determined from the gross earnings (salary/wages, taxable allowances, additional payments) in the Current or One Off Pay.

-

average gross taxable YTD - gross earnings are determined by averaging the gross taxable earning for the financial year to date over the number of pays received.