This document provides information on what Payroll Tax is in Australia and some examples on how its setup.

What is Payroll Tax?

Payroll tax is a self-assessed, general purpose state and territory tax assessed on wages paid or payable by an employer to its employees, when the total wage bill of an employer (or group of employers) exceeds a threshold amount. The payroll tax rates and thresholds vary between states and territories.

Returns are lodged, and payment of liability made, at an agreed frequency (monthly, quarterly, or annually) to the respective revenue office in the Australian state and/or territory in which the wage payment is deemed liable.

All Australian states and territories have harmonised a number of key areas of payroll tax administration. Information and Revenue Rulings on the harmonised key areas are accessible from this website.

Payroll Tax is not paid by the employee but paid by the Company. Most AU customers have a Payroll Tax On-Cost non-paying allowance and payroll rules setup

The Allowance can sometimes be a Hidden Allowance.

Harmonisation of Payroll Tax in Australia

Australian state and territory governments enacted legislation aligning payroll tax provisions in the following key areas:

-

timing of lodgement of returns;

-

motor vehicle allowances;

-

accommodation allowances;

-

a range of fringe benefits;

-

work performed outside a jurisdiction;

-

employee share acquisition schemes;

-

superannuation contributions for non-working directors; and

-

grouping of businesses.

Since 2007, six of the Australian states and territories have enacted harmonised (template) payroll tax legislation with Queensland amending their existing legislation by introducing aligned provisions in the key areas. Western Australia has enacted similar aligned provisions within their payroll tax legislation from 1 July 2012.

In addition to legislative harmony, Australian states and territories have also committed to greater administrative consistency. As a result:

Payroll Tax Revenue Rulings / Public Rulings / Circulars have been harmonised and published. Access to these publications is provided on the Revenue Rulings page.

Where an employer operates in more than one harmonised Australian state and territory, the relevant revenue offices will consult one another and share relevant taxpayer information in determining private rulings and objections matters.

For the purposes of administering state and territory taxation laws, information is exchanged with other revenue offices, and the Australian Taxation Office (ATO), to assist in the proper identification and accurate assessment of taxation liabilities.

In this regard the sharing of information with other revenue offices and the ATO across all taxation laws administered by the state or territory is carried out in accordance with the relevant Taxation Administration Act (TAA) enacted by the respective state or territory and under Schedule 1, Division 355-65 of the Commonwealth Taxation Administration Act 1953.

Compliance

Australian State and Territory Revenue Offices regularly conduct audits and investigations to ensure all liable employers are complying with their legal requirements under payroll tax legislation.

Each year large numbers of employers fail to register for payroll tax and are subject to penalties for the following reasons:

-

failing to register when total wages paid in a jurisdiction exceed that jurisdiction’s monthly threshold amount;

-

failing to register in each jurisdiction in which they pay wages;

-

failing to register a related entity under the grouping provisions, including:

-

where a holding / subsidiary relationship exists (mandatory grouping);

-

where two businesses are controlled by the same person or persons (e.g. common partners / shareholders / directors / beneficiaries or any combination of these);

-

the common use of employees.

-

Commonly identified areas that registered employers have issues with include:

-

failing to include all liable wages in the total wages calculation;(i.e. director’s fees; superannuation payments; taxable fringe benefits)

-

failing to declare fringe benefits and benefits under employee share schemes;

-

incorrectly claiming an exemption for certain wages;

-

incorrectly classifying employees as contractors;

-

late lodgement and / or payment of monthly or annual returns.(monthly due by the 7th day of following month; annual by 21st day of July)

-

failing to declare payments to portable long service leave and redundancy schemes (applicable in Western Australia and the Australian Capital Territory only) ;

Penalties are imposed if employers fail to register and when it is identified that an employer has provided false or misleading information in submitted payroll tax returns or in response to requests for information.

Recent statistics gathered from Australia-wide compliance activities identified that over 90% of involuntary payroll tax registrations fitted into one of the following four categories;

-

An employer’s total wages exceeded the threshold in a jurisdiction where they employ;

-

An employer was liable for payroll tax only when their interstate wages were taken into account;

-

A grouped employer was liable for payroll tax when the group’s combined Australia-wide wages were taken into account;

-

When wages paid to liable contractors were included, the total Australia-wide wages resulted in a liability for payroll tax.

Employers who voluntarily declare their liabilities may receive significantly lower penalties than those who do not.

Payroll Tax Rates

Victoria

1 July 2020 - 30 June 2021

4.85%

2.02% for regional Victorian employers

1.2125% for regional employers based in bushfire affected areas

Tasmania

1 July 2020 - 30 June 2021 Wages:

0 to 1250000 Rate: 0

1250001 to 2000000 Rate: 4

2000001 and above Rate: 6.1

ACT

1 July 2020 - 30 June 2021

$166,666.66 per month ($2,000,000 per year) Rate: 6.85

New South Wales

1 July 2020 - 30 June 2021

Threshold: $1,200,000 Rate: 4.85%

Queensland

1 July 2020 - 30 June 2021 The payroll tax rate is:

4.75% for employers or groups of employers who pay $6.5 million or less in Australian taxable wages

4.95% for employers or groups of employers who pay more than $6.5 million in Australian taxable wages.

Regional employers may be entitled to a 1% discount on the rate until 30 June 2023.

Northern Territory

1 July 2020 - 30 June 2021 Annual wage threshold $1,500,000

Monthly wage threshold $125,000 Rate: 5.5%

Western Australia

|

Annual Australian taxable wages |

Tax rate |

Calculation of tax payable |

|---|---|---|

|

1 July 2020 - when monthly Australian taxable wages are more than $83,333 |

||

|

More than $1 million but less than $7.5 million |

5.50% |

WA taxable wages - deductable amount x tax rate |

|

$7.5 million or more but not exceeding $100 million |

5.50% |

WA taxable wages

|

|

More than $100 million but not exceeding $1.5 billion* |

5.5% for wages up to

|

WA taxable wages

|

|

More than $1.5 billion* |

5.5% for wages up to

|

WA taxable wages

|

South Australia

|

Does not exceed |

Exceeds

|

Exceeds $1 million |

Exceeds

|

Exceeds

|

|

|---|---|---|---|---|---|

|

$600,000 |

but not $1 million |

but not $1.5 million |

|||

|

from 1

|

nil |

variable from 0% to 4.95% |

4.95% |

||

Payroll tax setup

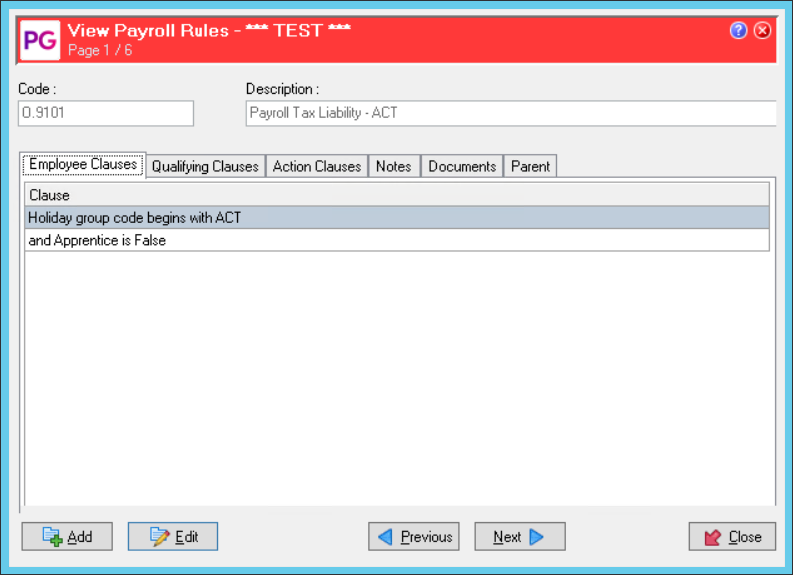

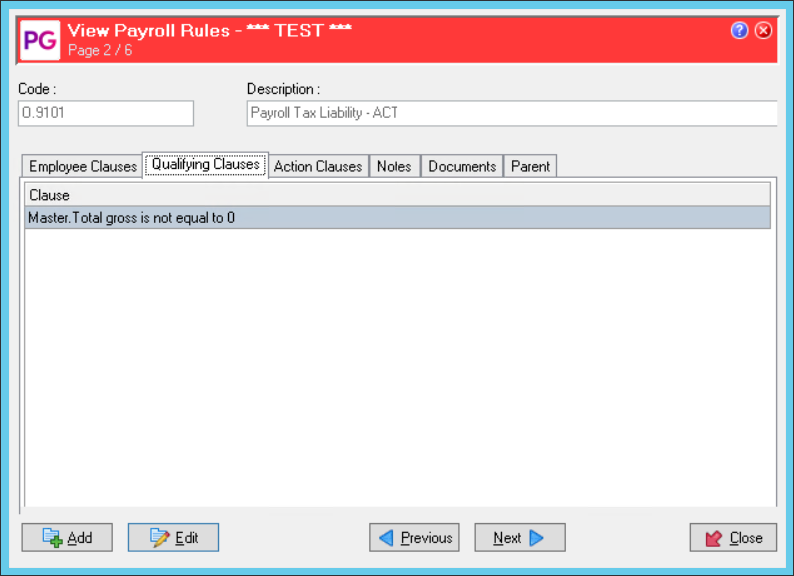

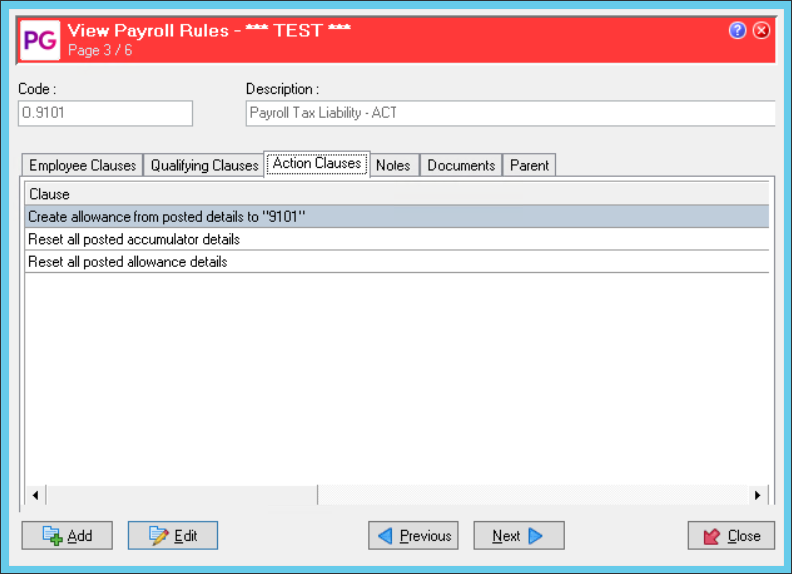

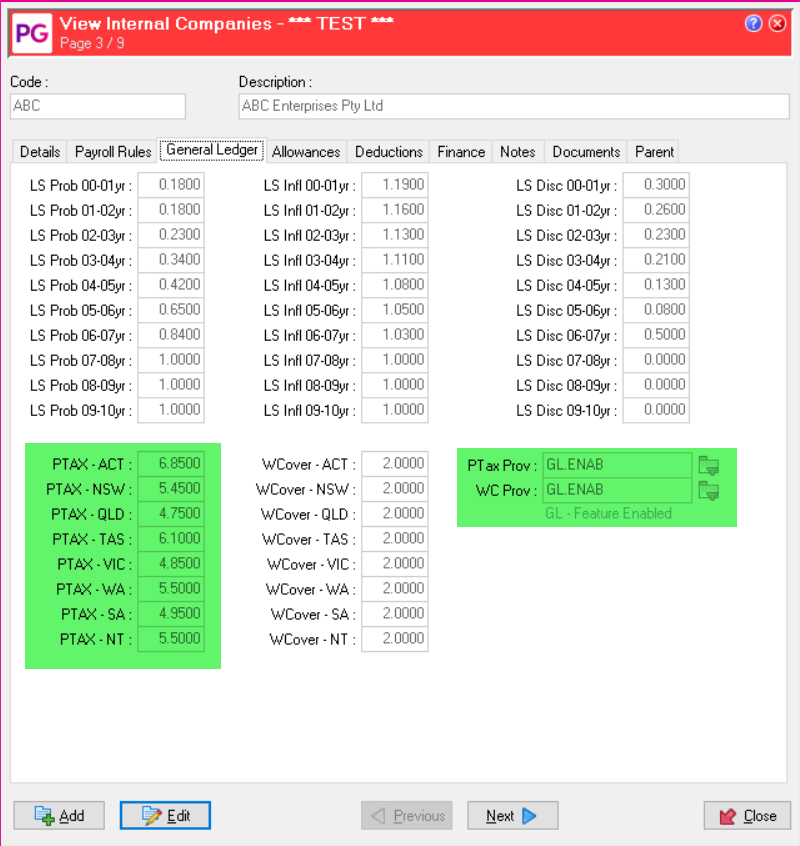

Example 1: Using Internal Companies

Some customers have the Payroll Tax Rates setup on the Internal Company then the Payroll Rules reference the rate.

See below:

Internal Company – General Ledger Tab:

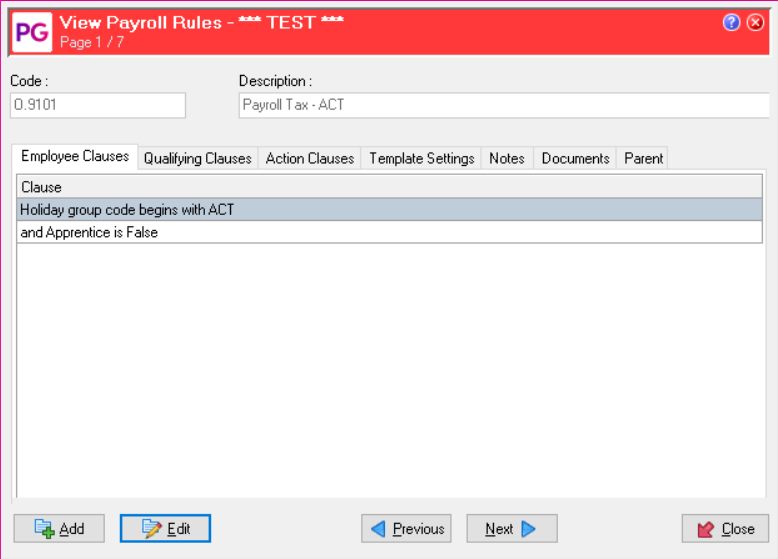

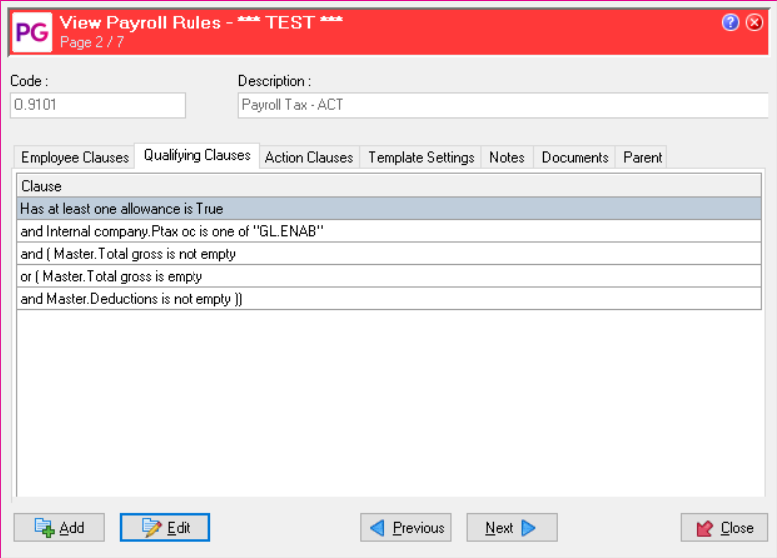

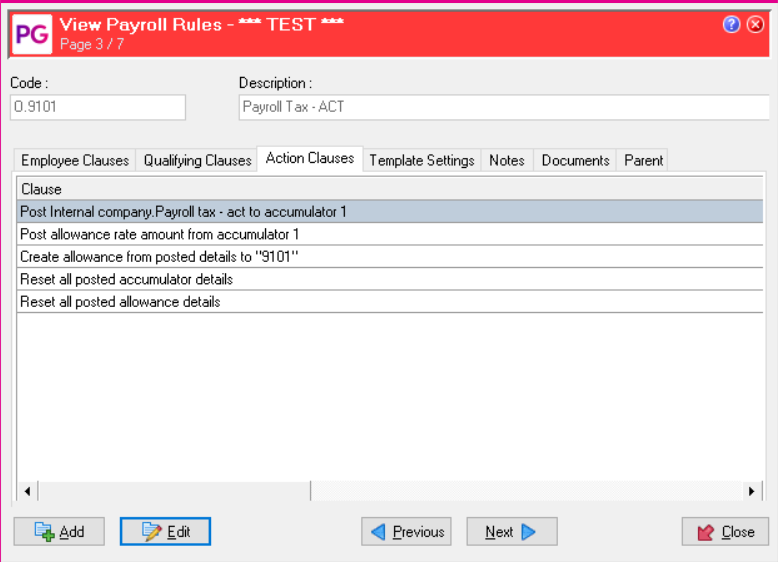

Payroll Tax ACT Payroll Rule:

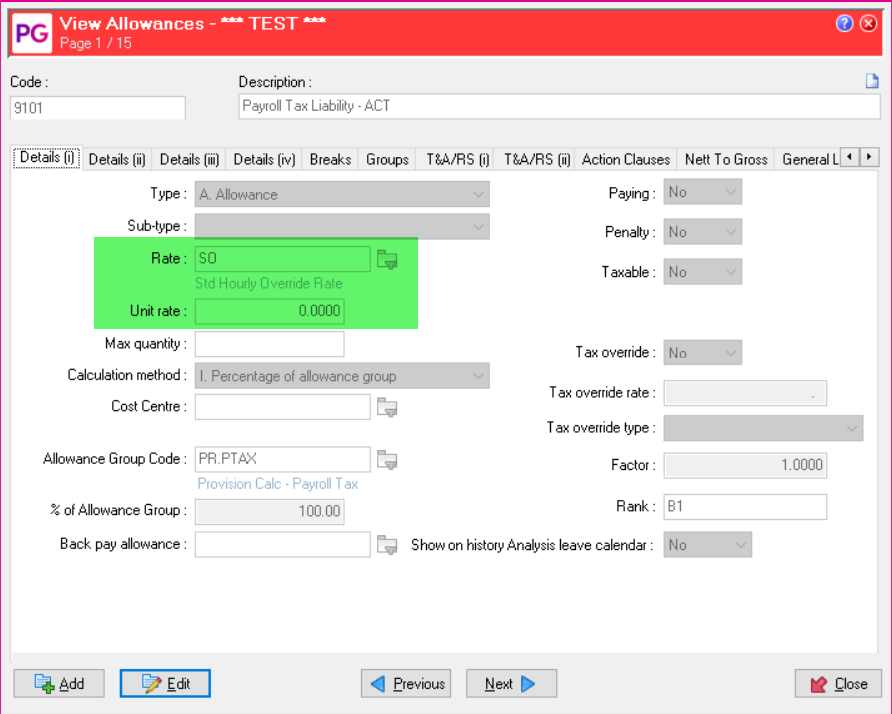

Payroll Tax ACT: Allowance Setup

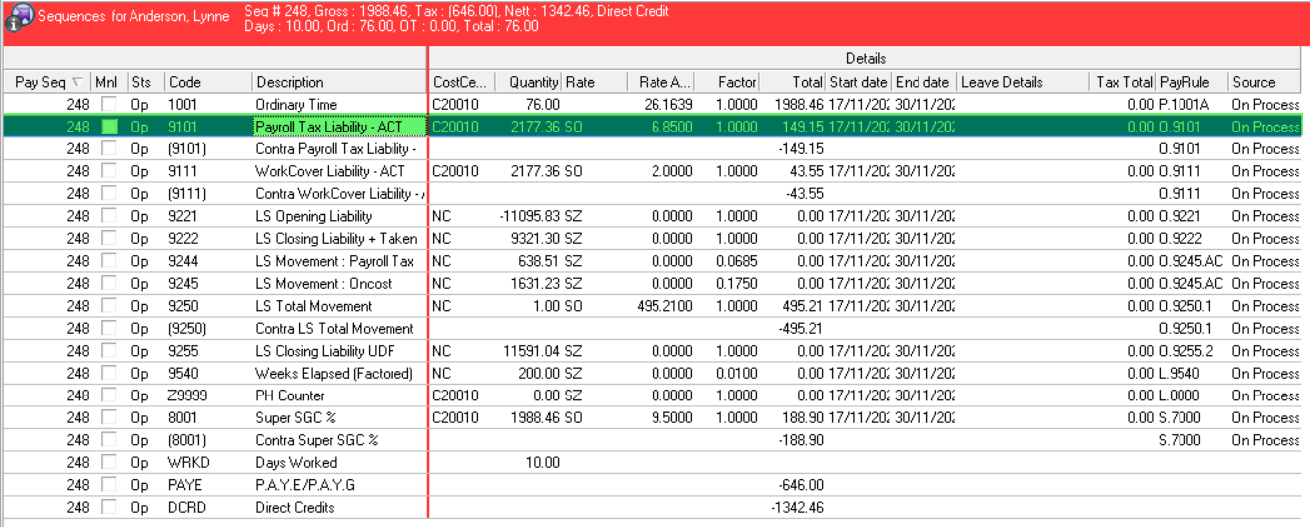

Transaction View Showing the Payroll Tax Liability – ACT allowance:

Example 2: Not Using Internal Companies

If Internal Companies are not used for the Payroll Tax calculation, the Payroll Tax Rate can be stored in the Actual Payroll Tax allowance.

See example below:

The payroll rule for generating this allowance may be similar to the below