How the Maximum Contributions Base works today

Before Payday Super (for pays with payment dates before 1 July 2026):

-

The Maximum Contributions Base is assessed each quarter, based on an employee’s OTE earnings for that quarter.

-

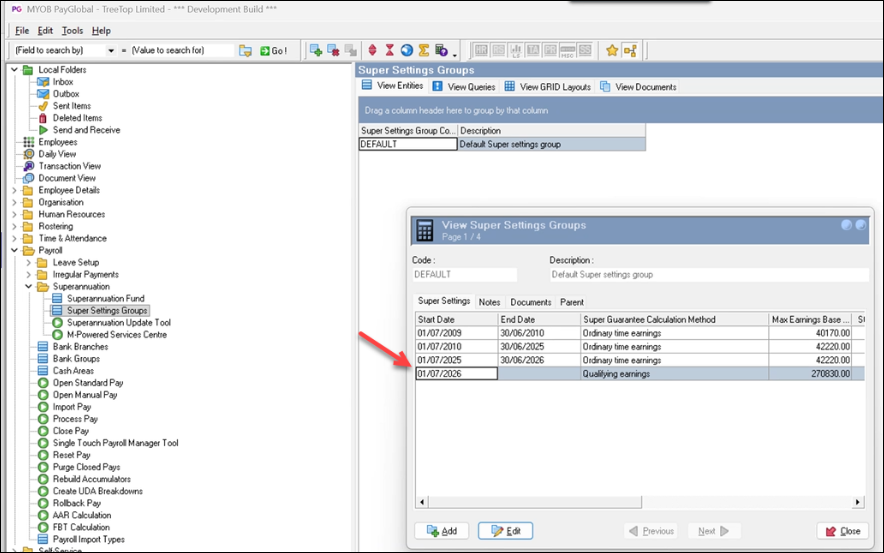

In PayGlobal, your Super Settings determine whether and how the MCB is applied, including the Max earnings base ($) amount and which allowances feed into that base.

How the Maximum Contributions Base changes under Payday Super

From 1 July 2026, the MCB will be assessed on an annual QE basis:

-

For pays with payment dates on or after 1 July 2026, the employee’s qualifying earnings (QE) for the current tax year to date are used to determine when they have reached the MCB.

-

When you create new Super Settings records with Start Dates on or after 1 July 2026, the Max earnings base ($) you enter should be the annual cap amount, not a quarterly amount.

-

This means that, for higher‑earning employees or those with large commission payments, they may reach the annual cap later (or earlier), depending on how their earnings are spread across the year.

PayGlobal will show a read‑only message on the Super Settings form to confirm which rule set applies—quarterly OTE vs annual QE—based on the payment date range you’re working with.

How PayGlobal helps you manage the MCB across the transition

-

Pre‑1 July 2026 – Quarterly OTE

-

Existing Super Settings records continue to use OTE earnings per quarter to determine when the MCB has been reached.

-

Only allowances with Use in Super OTE = Yes should feed into the Max earnings base calculation for pre‑1 July periods.

-

-

From 1 July 2026 – Annual QE

For new or updated Super Settings that apply from 1 July 2026:

-

Ensure that the Max earnings base ($) value you enter is the annual MCB amount for that tax year.

-

Only allowances with Use in Super Qualifying Earnings = Yes should feed into the Max earnings base calculation for post‑1 July periods.

-

Use Transaction View’s Super Qualifying Earnings column and your updated reports to verify when employees approach or reach the cap over the course of the year.

-

Worked example – quarterly OTE vs annual QE

Example (illustrative only – confirm figures with current ATO thresholds)

-

In 2025–26, an employee’s OTE each quarter is high and relatively stable. They reach the quarterly OTE‑based MCB partway through each quarter, and your SG calculations stop at the quarterly cap.

-

From 1 July 2026, the same employee’s earnings are treated as QE, and the cap is assessed over the full tax year. If their earnings are more variable (for example, if large commissions are paid late in the year), they may cross the annual QE‑based cap at a different point than they previously crossed the quarterly OTE‑based cap.

By using the new QE fields and updated Super Settings, you can track how close employees are to the annual QE‑based MCB and ensure SG is being calculated as expected.

What you should review

-

Check your existing Super Settings to confirm:

-

How your Max earnings base ($) is currently set.

-

Which allowances feed into the MCB calculation, and whether they align with the ATO’s OTE/QE definitions. Refer to Check your PayGlobal setup for Payday Super (QE)

-

-

Plan how you will transition to annual QE‑based MCB from 1 July 2026, including:

-

Updating Max earnings base ($) to the correct annual amount in new Super Settings records.

-

Ensuring the Use in Super Qualifying Earnings flags on allowances are correctly set so that only in‑scope payments contribute to the MCB.

-

-

For complex arrangements under awards or enterprise agreements, confirm your approach with the ATO, your tax adviser or payroll advisor, and consider engaging MYOB Professional Services if you need help reviewing your configuration.