|

Payment Type |

Termination Reason |

Leave Accrual Period* |

PAYG Calculation |

Where on Payment Summary |

|---|---|---|---|---|

|

Annual Leave |

Bona Fide Redundancy Approved Early Retirement Invalidity Only All Other |

All Annual Leave

Pre 18/08/1993 Post 17/08/1993 |

Taxed at 31.5%

Taxed at 31.5% Taxed at marginal rates |

Lump Sum Payment A

Lump Sum Payment A Salary, Wages, Bonus etc. |

|

Annual Leave Loading |

Bona Fide Redundancy Approved Early Retirement Invalidity Only All Other |

Pre 18/08/1993 Post 17/08/1993 |

Excess over $320 taxed at 31.5%

Excess over $320 taxed at marginal rates |

Lump Sum Payment A

Salary, Wages, Bonus etc. |

|

Long Service Leave |

Bona Fide Redundancy Approved Early Retirement

All Other |

Pre 16/08/1978 Post 18/08/1978

Post 16/08/1978 to 17/08/1993 Post 17/08/1993 |

5% of value taxed at marginal rates Taxed at 31.5% 5% of value taxed at marginal rates Taxed at 31.5% Taxed at marginal rates |

Lump Sum Payment B Lump Sum Payment A Lump Sum Payment B Lump Sum Payment A Salary, Wages, Bonus etc. |

|

Bona Fide Redundancy & Approved Early Retirement Scheme Payments |

Up to $7,732.00 + ($3,867.00 per completed service year) Payment in excess of above calculation is paid as ETP (see below) |

Nil Tax |

Lump Sum Payment D |

|

|

Eligible Termination Payments (ETPs) – Employer Payments |

Lieu of Notice Payments Ex Gratia Payments (Golden Handshake) Sick Leave (if applicable) RDO Accrual Invalidity Payments Excess part of Redundancy & Approved Early Retirement Scheme Payments (over Lump Sum D Limit) Any other Termination Payments not falling in Salary & Wages, Lump Sum Payments A, B or D |

Pre 01/07/1983 component Post 30/06/1983–Employee 55+

|

Nil Tax 15.5% up to $140,000.00, thereafter 31.5% Taxed at 31.5% |

ETP Payment Summary ETP Payment Summary ETP Payment Summary |

Notes

Marginal Rates

The following calculation method is used for marginal rates:

$ Value / No of pay periods per year This is irrespective the employee's service (Weekly - 52, Fortnightly - 26, Monthly - 12)

Add this value to the employee's average earnings for the current tax year

Determine the tax on this 'new' value

Deduct this tax value from the tax on the average pay

Multiply this value by No of Pay Periods per year

This is the tax to be deducted from the $ Value

E.g. $10 000-00 / 52 = $192.31

Average Pay: $600

New Pay: $792.31

Tax on New Pay: $173

Tax on Ave Pay: $112

Difference: $61

$61 * 52 = $3172-00

Tax deducted from $10,000-00 = $3172-00

ETP Component - Post 06/1994 Invalidity component

This is based on the employee's service period.

Post 06/1994 A x B A = Total Amount of ETP

C B = No of whole days from termination to date on which employee would have retired

C = Aggregate of whole number of days in service period for ETP and "B"

Pre 01/07/1983 Component

No of days services from Start Date to 01/07/1983 X ETP Amount minus post 06/1994 Invalidity component

Total days service

This value is not subject to PAYG

Post 30/06/1983 Component - Untaxed Element

Post 06/1983 service days X ETP Amount minus Post 06/1994 Invalidity Component

Total service days

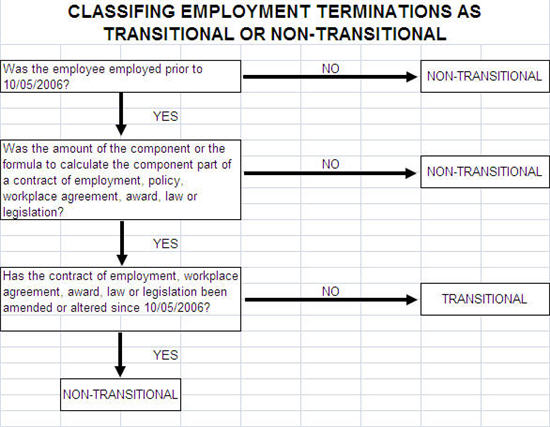

Classifying employment terminations

On termination, leave is paid as accrued up to the TERMINATION DATE.

Need more help? You can open the online help by pressing F1 on your keyboard while in your software.

You can also find more help resources on the MYOB Exo Employer Services Education Centre for Australia or New Zealand.