Setting up employees for KiwiSaver

Whether you're setting up KiwiSaver for a new employee or an existing one, each employee's scenario will have different requirements. This page describes these scenarios and how to select the right settings for each one. You also need to set up your employer contribution settings for each employee.

Employee KiwiSaver settings

New employees

Go to the Pay Details screen (MPPP2310).

In the Employee ID field, select the employee whose KiwiSaver you want to set up.

On the KiwiSaver tab, add a new row by clicking the + button.

The Date of Change will be the system business date (change this if necessary).

Under KiwiSaver Eligibility, select “New Employee”

The other settings you need to select depend on the employee's specific scenario.

If the employee will be receiving income that is exempt from KiwiSaver, under Income Exempt from KiwiSaver, select the reason for the exemption. If more than one reason applies, select the reason that accounts for the greater part of the employee’s pay. Choose from:

Board-lodging

Taxable allowances accommodation

Voluntary Bonding Scheme

Retiring allowance

Overpayment of employer’s super cash contribution

Honoraria payments

The other columns will not be editable for a new employee.

On the form toolbar, click the Save icon (:ADV_Save:).

Existing employees

The Pay Details KiwiSaver tab must also be updated in the following scenarios for existing employees:

Opting in to KiwiSaver:

Add a new row by clicking the + button.

The Date of Change will be the system business date (change this if necessary).

Under KiwiSaver Eligibility, select “Existing employee opt-in”.

Opting out of KiwiSaver:

Add a new row by clicking the + button.

The Date of Change will be the system business date; this must be the date the employee signed/provided the Opt out form.

If the new employee has already been reported, then leave KiwiSaver Eligibility and KiwiSaver Status blank.

Under Opted out of KiwiSaver, tick the checkbox

If the Date of Change is past the standard (employment start date plus 56 days), a Late Opt-out reason must be selected:

Employer didn’t provide info pack by start date = 7 days

IRD didn’t send investment statement upon allocation to a default scheme

Employer didn’t provide investment statement for default scheme

Events outside of control prevented submission of opt-out application within 56 days

Didn’t meet criteria to join KS

Incorrectly enrolled under age 18.

Other

If the Late Opt-out reason is “Other”, a description must be entered under Other description (up to 500 characters).

Casual employee converted to permanent employee after 28 days, not previously enrolled in KiwiSaver:

Add a new row by clicking the + button.

The Date of Change will be the system business date (change this if necessary).

Under KiwiSaver Eligibility, select “Existing employee auto enrol”.

ND tax code with no IRD number, replaced by a different tax code and an IRD number:

If an employee has been reported with no IRD number, and the IRD number is subsequently provided, the Pay Details Taxation tab will display a message advising that this change will be reported in Payday filing.

The Employee Details file will include two entries:

Tax code ND with no IRD number, the date of the change will be reported as the IRD Update Date.

New tax code with IRD number, Start Date will report the employment start date.

Employee Transfer:

If the employee is being transferred from one branch to another where the branch IRD number is different, then this must be reported in payday filing as if the employee is departing and a new employee. This must be done manually in myIR.

Scenarios that don’t require changes

Employer super contributions

For more information, see these IRD resources:

Page 16 of IRD Employer’s guide – IR335.

Set employer super contributions

Go to the Pay Details screen (MPPP2310).

In the Employee ID field, select the employee you want to set up employer super contributions for.

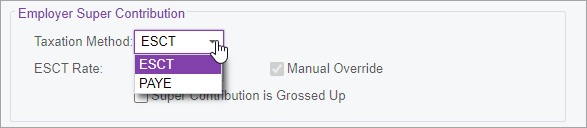

On the Taxation tab, choose the Employer Super Contribution settings:

Taxation Method – Select either ESCT or PAYE. All employer contributions paid to a superannuation fund, including KiwiSaver schemes and complying funds, are liable for ESCT (employer superannuation contribution tax). The exception to this is if the employee and employer have agreed to treat some or all of the employer contribution as salary or wages under the PAYE rules.

ESCT Rate – If you selected ESCT as the Taxation Method, you need to select a rate. The ESCT rate is based on the employee's salary or wages plus gross superannuation employer contributions received in the previous tax year, 1 April to 31 March. For more information, see page 19 of IRD Employer’s guide – IR335.

Super Contribution is Grossed Up – Sometimes, an employer may be "locked in" to an employment agreement where they contribute a set percentage of their employee's salary. In this case, you might need to gross up the employer contribution so the employee receives their full entitlement.

If you select this checkbox, the net employer contribution is the 3% employer contribution.

If you don't select this checkbox, the net employer contribution is 3% employer contribution minus ESCT / PAYE on Employer Super.

On the form toolbar, click the Save icon (:ADV_Save:).

Example employer super contributions

Example | Scenarios | Super Contribution is Grossed Up is selected Net employer super is set % of income | Super Contribution is Grossed Up is not selected Net employer super has tax removed |

|---|---|---|---|

Gross Income = 1000 Tax code = M / 30% Employee contribution 3% Employer contribution 3% Calculations are detailed in pg6 of IRD Employer’s guide - IR335. | Taxation Method = ESCT of 10.5% Standard scenario. PAYE calculated on | Employee Super = 30 Employer Super = 30 Net Employer Super = 30 PAYE = 181 (no impact) ESCT = 3.51 | Employee Super = 30 Employer Super = 30 Net Employer Super = 26.85 (30 - ESCT) PAYE = 181 (no impact) ESCT = 3.15 |

Taxation Method = PAYE Exception: Employee and employer have agreed to treat the employer contribution as salary or wages under the PAYE rules. | Employee Super = 30 Employer Super = 30 Net Employer Super = 30 PAYE on Employer Super = 9 PAYE = 190 (181+9) ESCT = 0 | Employee Super = 30 Employer Super = 30 Net Employer Super = 21 (30 - PAYE) PAYE on Employer Super = 9 PAYE = 190 (181 + 9) ESCT = 0 |