This page explains the compliance changes related to MYOB Acumatica — Payroll for the 2024-25 tax year, along with procedures for supervisors or payroll administrators to prepare for the new tax year in MYOB Acumatica — Payroll.

If you'd like help with your end of tax year procedures, contact your MYOB Acumatica — Payroll consultant or email csenterprise@myob.com to book one of ours.

Compliance changes for the 2024-25 tax year

Below is the list of Inland Revenue (IR) changes for the New Zealand tax year 2024-2025, effective from 1st April 2024. There have been no changes to Kiwisaver or payday filing.

For full details, see Tax rates for individuals on the IR website.

To keep you compliant, when you open a pay with a physical pay date of 31 July 2024 or later, MYOB Acumatica — Payroll automatically applies these new tax rates and thresholds.

End of tax year procedures for 2024

MYOB Acumatica — Payroll automatically updates some rates and thresholds to keep you compliant. However, you need to manually update minimum wage rates, the work calendar and ESCT rates. These manual updates are part of the end of tax year procedures in MYOB Acumatica — Payroll, which are all explained below.

To get started with these procedures, make sure you complete and close all pays for the tax year being updated.

You must complete these procedures before closing your first pay with a payment date in the new tax year.

2. Review default rates

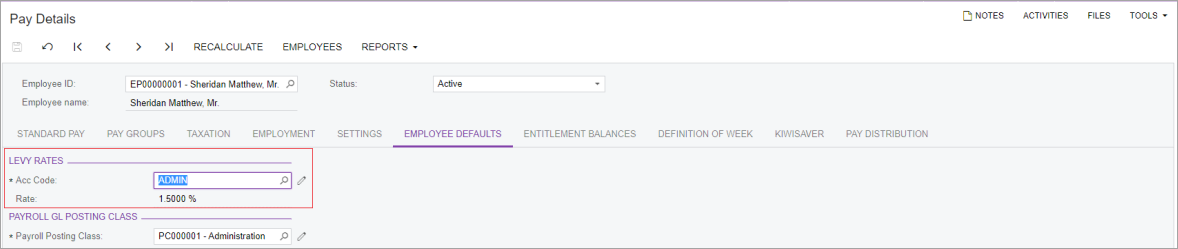

Business ACC default rates

If you use MYOB Acumatica — Payroll for managing general ledgers, it's good to check if your business's default Business ACC Rates and Business Classification Codes (BIC) or Classification Units (CU) are up to date.

Business ACC Levy Rates aren't the same as ACC Levy rates, which are used as part of tax calculations for an employee. For more details, see Calculating your levies.

You can check these on the ACC Rates screen.

You can then change the employee's ACC code on the Employee Defaults tab of the Pay Details screen.

Pay item and standard pay settings

If your company's financial year is same as its tax year, check your employee pay item and standard pay settings are up to date.

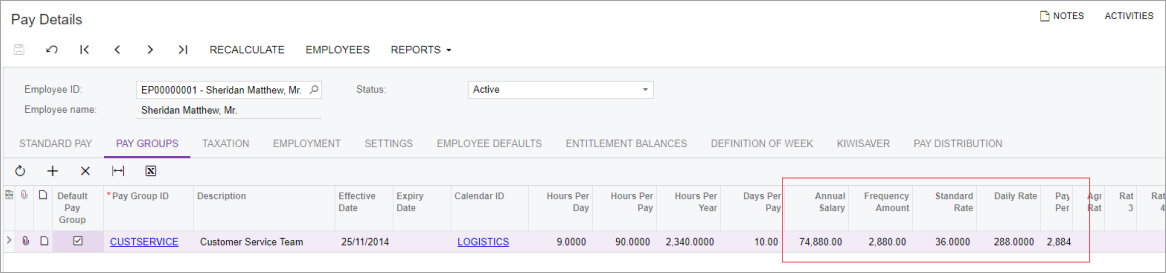

3. Meet minimum wage requirements

On the Pay Group tab of the Pay Details screen or the Employee's Current Pay screen, you can check if your employees' salaries and rates are above minimum wage limits.

If you use MYOB Acumatica — Workforce Management and need to update minimum wage rates part-way through a pay period, see our help page on how to do so.

The Pay Activity Details Data report is helpful when verifying that your employees' rates comply with the minimum wage rate for the new tax year. It can also help identify which employees might need their salary/wage rates revised.

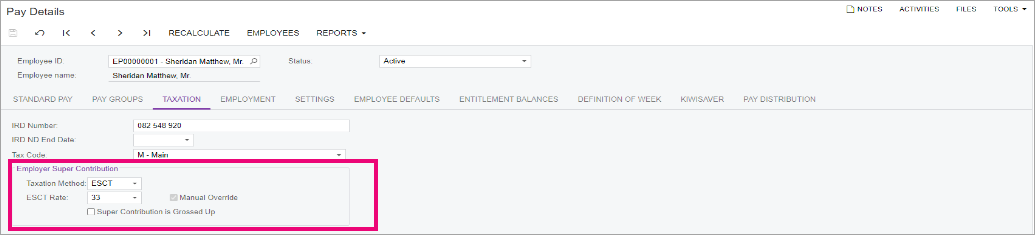

4. Recalculate ESCT rates

At the beginning of each tax year, you need to work out the ESCT rates for your staff. This varies for each employee, as it’s based on their salary or wage for the previous year plus their employer contribution.

The new ESCT report can help you calculate your employee's ESCT rates for the next tax year.

ESCT rates aren't automatically calculated in MYOB Acumatica — Payroll. So, before you open the first pay of the new tax year, make sure you calculate ESCT rate and update them on the Taxation tab of the Pay Details screen.

Once you calculate an employee's ESCT rate, it remains the same for the whole tax year, even if there are changes to their salary or wages during the tax year.

If an employee worked for you for the entire previous tax year

When an employee's start date is before the previous tax year's start date, then their ESCT rate depends on ESCT threshold value, which you can calculate using the following formula:

ESCT Threshold = Total Gross Income in Previous Tax Year + Total Gross Employer’s Superannuation Contributions in Previous Tax Year.

If an employee started in the middle of the previous tax year

If an employee's start date is after the previous tax year's start date, but before the start of the current tax year, their ESCT rate value is based on their expected income for the current tax year:

ESCT Threshold = (Estimated Gross Income per pay for current Tax Year + Estimated Gross Employer’s Superannuation Contributions per pay for current Tax Year) / Number of days in the pay frequency in current Tax Year * Number days in current Tax Year (i.e. 365).

If an employee started in the middle of the current tax year

For employees starting in the middle of the current tax year (not the previous tax year), ESCT Rates for those employees for the current tax year are expected to be set as part of their onboarding process, as per the IR page on deducting ESCT from each employer contribution.

5. Update public holiday dates on the work calendar

Every year, you need to add the coming year's public holidays to your employee work calendars. There are no mondayised holidays in the 2024-25 tax year.

For details of the 2024 and 2025 public holidays, see Employment New Zealand – Public holidays and anniversary dates.

When you update a work calendar, it impacts all employees that use the same calendar. If you only want to make changes for certain employees, you can create a new calendar for them with desired settings. For more details, see the annual leave white paper.

Adding a public holiday to a work calendar

-

Go to the Work Calendar form (CS209000).

-

Select the calendar you want to update.

-

Click the Exceptions tab.

-

Click the Add Row button.

-

In the new row, enter the date for the holiday.

-

Complete the Description field, Start Time and End Time fields.

-

On the form toolbar, click the Save icon.

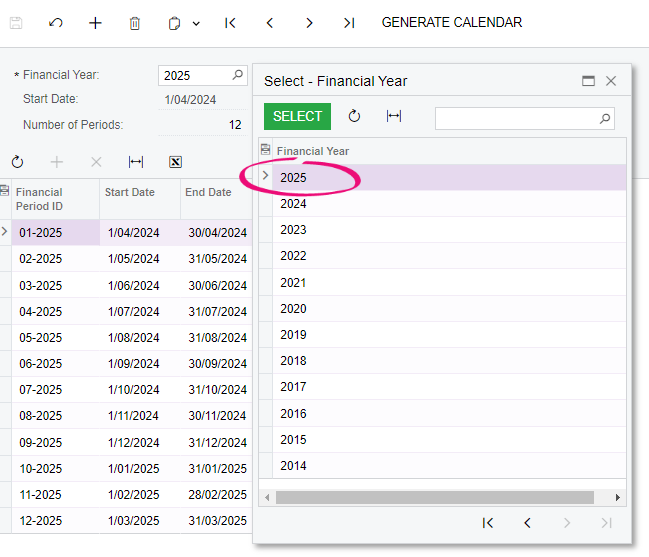

6. Check financial calendars

You can follow these steps on either the Master Financial Calendar screen or the Company Financial Calendar screen, depending on how your site is set up.

You need to have a financial calendar with open periods for the 2024–25 tax year. In the Financial Year field, make sure you have a 2025 calendar.

If you don’t have a 2025 calendar, generate one

-

Click Generate Calendar on the form toolbar.

-

In the Generate GL Calendar window:

-

Set the From Year to 2024.

-

Set the To Year to 2025.

-

-

Click OK.

Open the periods for the 2025 calendar

-

In the Financial Year field, select the 2025 calendar.

-

On the form toolbar, click the three dots icon … and choose Open Periods. The Manage Financial Periods form (GL503000) opens.

-

If the Status column shows the periods are Inactive, you need to open them. Select Close from the Action dropdown.

-

Set the To Year field to 2025.

-

On the form toolbar, click Process All.