This page explains the compliance changes for the 2024-25 financial year, and how to prepare for them in MYOB Acumatica — Payroll.

For supervisors or payroll administrators who run end of financial year procedures, you'll also find how to finalise up the 2023-24 year.

Some of the ATO articles that this page links to might not reflect the new compliance changes. These ATO articles will likely be up-to-date by mid-June.

Compliance changes for 2024-25

The following changes come into effect on 1 July 2024. In most cases, the new rates and thresholds are applied automatically when you open a pay with a physical pay date of 1 July 2024 or later.

For more details, see Tax tables on the ATO website.

PAYG

For Australian residents

Tax rates have changed.

-

On income between $18,201 and $45,000, the rate has reduced from 19% to 16%.

-

On income between $45,001 and $135,000, the rate has reduced from 32.5% to 30%

-

A 45% rate now only applies to income over $190,000. Previously, it applied to income over $180,000.

The following table explains how much tax is paid on different incomes. The table doesn’t include the Medicare levy or any low income or middle income offsets.

|

Taxable income |

Tax on this income |

|---|---|

|

0 to $18,200 |

Nil |

|

$18,201 to $45,000 |

16 cents for each $1 |

|

$45,001 to $135,000 |

$4,288 plus 30 cents for each $1 |

|

$135,001 to $190,000 |

$31,288 plus 37 cents for each $1 |

|

over $190,000 |

$51,638 plus 45 cents for each $1 |

Non-resident PAYG tax rates and thresholds

The following table explains how much tax is paid on different incomes. Non-residents don’t pay the Medicare levy.

|

Taxable income |

Tax on this income |

|---|---|

|

$0 to $135,000 |

30 cents for each $1 |

|

$135,001 to $190,000 |

$40,500 plus 37 cents for each $1 |

|

$190,001 and over |

$60,850 plus 45 cents for each $1 |

Shearing and horticultural industries

For foreign residents who provide a TFN, the tax rate has reduced from 32.5% to 30%. For more details, see the tax table for individuals employed in the shearing and horticultural industry on the ATO website.

Medicare levy exemptions for seniors and pensioner

Tax tables for seniors and pensioners now include full and half Medicare levy exemptions for the three payee categories: single, illness separated and couple. For more information, see tax tables for seniors and pensioners on the ATO website.

We’re adding support for this change in the upcoming 2023.1.5 release of MYOB Acumatica — Payroll.

Working holiday makers (WHMs)

If you're registered as an employer of WHMs, the following table explains tax rates for WHMs.

If you’re not registered as an employer of WHMs, you need to apply foreign resident withholding rates.

|

Taxable income |

Tax on this income |

|---|---|

|

$0 to $45,000 |

15 cents for each $1 |

|

$45,001 to $135,000 |

30 cents for each $1 |

|

$135,001 to $190,000 |

37 cents for each $1 |

|

$190,001 and over |

45 cents for each $1 |

If WHMs don’t provide a tax file number, you must withhold at 45% on total payments made.

Return-to-work payments

For any employee who receives a payment to resume working or provide services, the withholding rate has reduced from 34.5% to 32%.

We’re adding support for this change in the upcoming 2023.1.5 release of MYOB Acumatica — Payroll.

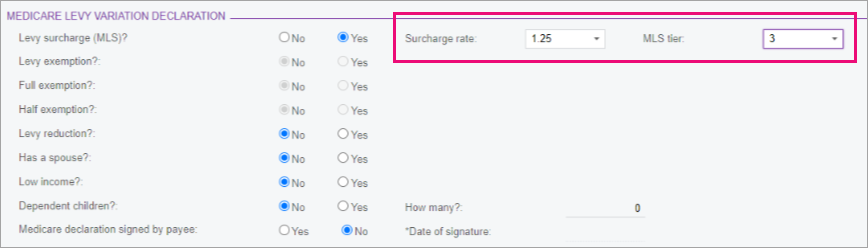

Medicare levy surcharge thresholds

From July 1 2024, Medicare levy surcharge thresholds are increasing. For details of the changes, see the ATO Medicare levy surcharge income, thresholds and rates page.

If any of your employees' Medicare levy surcharge changes as a result of the new thresholds, update their pay details:

-

Go to the Pay Details form (MPP3120).

-

Select the employee, and open the Taxation tab.

-

In the Medicare Levy Variation Declaration section, select the new Surcharge rate and MLS tier. If the employee is no longer required to pay a surcharge, select No for Levy surcharge (MLS)?

-

Save the record.

Student loans

There are no changes to the minimum student loan rates, but repayment thresholds are increasing, with the minimum repayment threshold changing from $51,532 to $54,435.

For full details of the new thresholds, see the Australian government's StudyAssist website.

This change will be automatically applied to all pays with physical pay date of 1 July 2024 or later.

Employee termination payments (ETP)

Employment Termination Payment (ETP) threshold amounts have changed for the 2024–25 financial year:

-

Life benefit termination payments ETP cap increases from $235,000 to $245,000.

-

For genuine redundancy and early retirement scheme payment limits:

-

The base limit has increased from $11,985 to $12,524.

-

The limit for each year of service has increased to $5,994 to $6,264.

-

This change will be automatically applied to all pays with physical pay date of 1 July 2024 or later.

Superannuation

Super guarantee

The compulsory superannuation guarantee rate increases from 11% to 11.5%.

Maximum super base contributions

The income per quarter increases from $62,270 to $65,070.

This is the maximum limit on an employee's earnings base for each quarter of any financial year. As an employer, you don't have to provide the minimum support for the portion of earnings above this limit.

These changes will be automatically applied to all pays with physical pay date of 1 July 2024 or later.

Child support deductions

From 1 January 2024 to 31 December 2024, the Child Support Protected Earnings Amount (PEA) are as follows:

|

Frequency |

Amount |

|---|---|

|

Weekly |

$514.50 |

|

Fortnightly |

$1,029.00 |

|

Four weekly |

$2,058.00 |

|

Monthly |

$2,237.16 |

Unused leave on termination of employment

There are no changes to withholding rates on unused leave on termination for 2024–2025. For the current rates, see the ATO website.

Fringe benefits tax (FBT)

There are no changes to FBT for 2024–2025. For information on the current rates and thresholds, see the ATO website.

Wrapping up the 2023–24 financial year

MYOB Acumatica — Payroll automatically updates some rates and thresholds to keep you compliant. However, you need to manually set up fringe benefits and Single Touch Payroll Phase 2.

To get started with these procedures, make sure you complete and close all pays for the tax year being updated.

You must complete these procedures before closing your first pay of the new tax year.

1. Verify your data and system setup

Check company and contact details

Company ABNs

On the SBR Registration tab of the Payroll Preferences screen (MPPP1100), make sure that each company has an ABN and software ID.

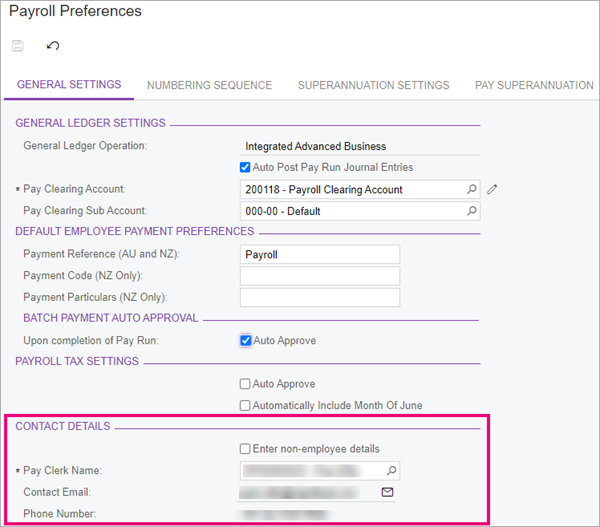

Contact details

On the General Settings tab of the Payroll Preferences screen, make sure that the contact details are correct for the person in your company who's in touch with the ATO.

Company data

Make sure that the details on the Companies screen are correct (CS1015PL).

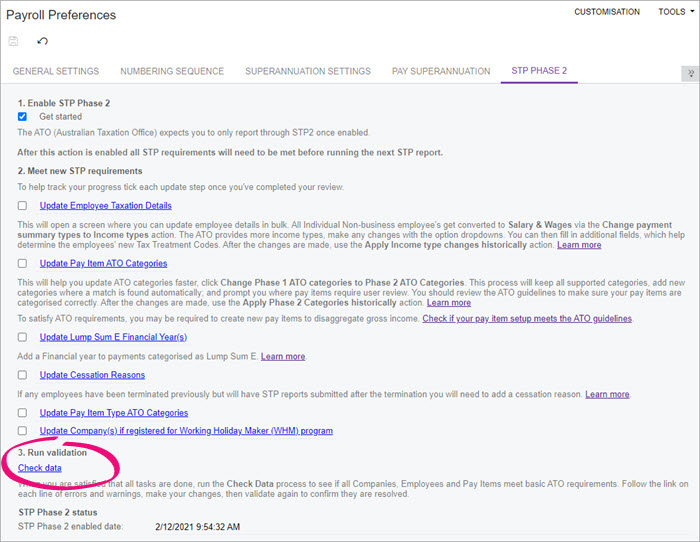

Also, MYOB Acumatica — Payroll has a feature to check for errors in your data. Although this feature was introduced to validate data for Single Touch Payroll, you can also use it to before the start of a new financial year. There are two places in MYOB Acumatica — Payroll where you can use this feature.

-

If you're using STP Phase 1, you can use the Check Company Data screen (MPPP5020).

-

If you're using STP Phase 2, you can click Check data on the STP Phase 2 tab of the Payroll Preferences screen (MPPP1100)

3. Reporting fringe benefits

If you have employees with reportable fringe benefits, you need to report these to the ATO via an STP pay event. This section explains how to:

-

Set up MYOB Acumatica — Payroll for reporting exempt and non-exempt fringe benefit payments.

-

Load reportable fringe benefits amounts.

-

Send the pay event data to the ATO after completing the reportable fringe benefits pay run.

Create a fringe benefit pay item type

By default, MYOB Acumatica — Payroll includes a Fringe Benefit Reporting pay item type, which you can assign to fringe benefit pay items that are liable for payroll tax. However, you need to create another pay item type for fringe benefits that aren't liable for payroll tax.

-

Go to the Pay Item Types screen (MPPP2160).

-

On the form toolbar, click the Add Row icon :ADV_Plus: .

-

Complete the Pay Item Type ID, Pay Item Type and Description fields.

-

Leave the Payroll Tax Liable checkbox unselected.

-

On the form toolbar, click the Save icon :ADV-Save: .

Create fringe benefit pay items

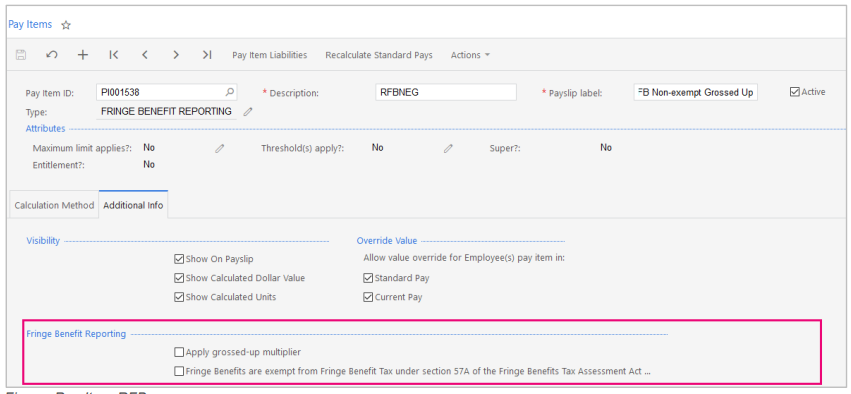

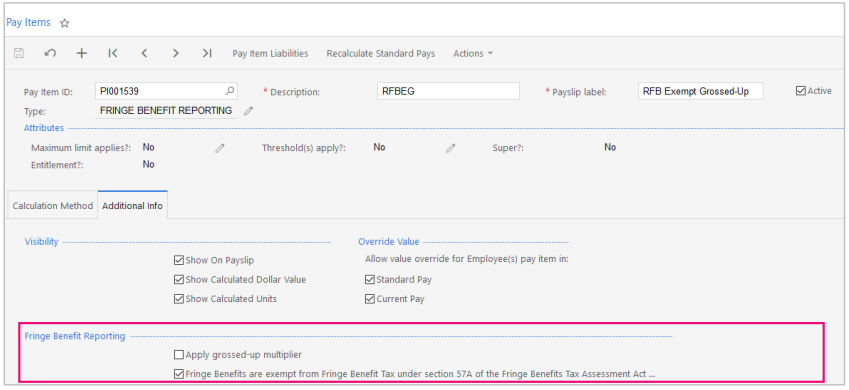

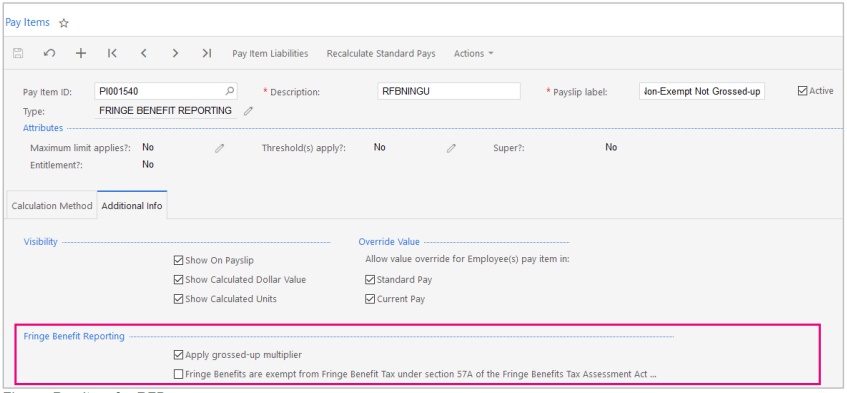

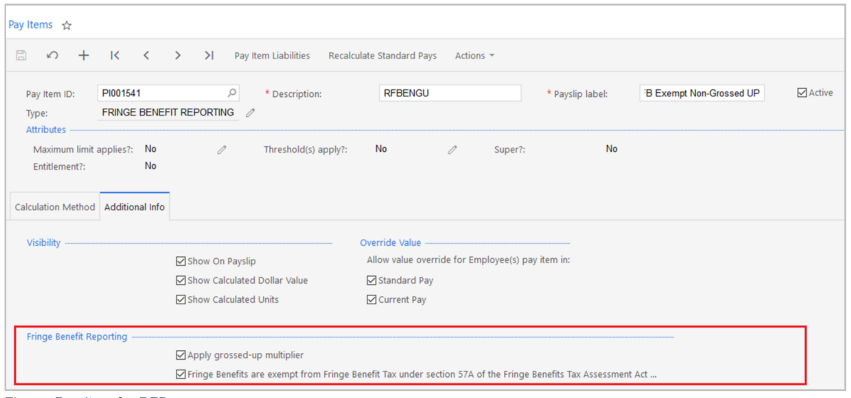

To correctly update MYOB Acumatica — Payroll for reportable fringe benefits, you'll need up to four pay items with different settings for how the amounts will be reported.

The table below shows which settings to select for different types of reportable fringe benefits. You can select these settings on the Additional Info tab of the Pay Items screen (MPPP2210).

Need a refresher on creating a pay item? See the Creating a pay item support article.

|

Type of reportable fringe benefit |

Pay item settings |

|---|---|

|

|

|

|

|

|

|

|

Update reportable fringe benefit amounts

The fringe benefit tax year is from April 1 2023 to March 31 2024. The Pay Period End Date should be no later than March 31 2024.

If the Pay Period End date is after March 31 2024, the reportable fringe benefit won't appear in the correct fringe benefit tax year.

The Physical Pay Date needs to be in June 2024, otherwise the pay event sent to the ATO will be rejected.

Employees can only be added to a current pay run on the fly if their pay frequency matches the pay run frequency. If they are added to a current pay run, then the standard pay of that frequency is brought into the pay run. To avoid having to go into each employee and manually delete the pay elements, we recommend adopting the following workflow to update reportable fringe benefits.

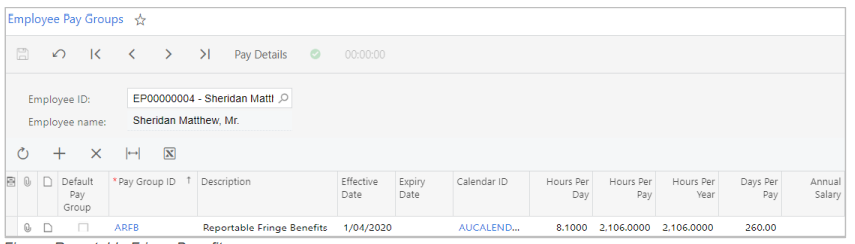

In this workflow, the fringe benefit amounts will be updated using a new pay group with the Pay Frequency set to Annually.

-

Go to the Pay Groups screen (MPPP2710).

-

On the form toolbar, click the Add Row icon :ADV_Plus: .

-

In the new row, complete the fields as follows:

-

Pay Group ID – ARFB

-

Description – Reportable Fringe Benefits

-

Hours per Day – 0.0000

-

Hours per Pay – 0.0000

-

Hours per Year – 0.0000

-

Pay Frequency – Annually

-

Pay Default – N/A

-

Last Pay Period Start Date – 01/04/2022

-

Last Pay Period End Date – 31/03/2023

-

Last Physical Pay Date – 21/06/2023

-

Active – click if yes

-

-

Go to the Employee Pay Groups screen (MPPP2250).

-

Add the ARFB pay group you created to each employee to be updated.

-

Select the Employee from the search window or enter the Employee ID.

-

Add the new Reportable Fringe Benefits pay group.

You can go into each Pay Details for each employee attached to the Reportable Fringe Benefit pay group and add the Pay Item to the Standard Pay or you can add the pay item to a current pay on the fly.

-

Load reportable fringe benefit amounts

-

Once all the employees have been updated then go to the Manage Pays form (MPPP4110) and from the Actions dropdown list Create Pay.

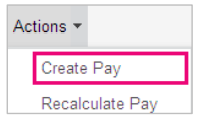

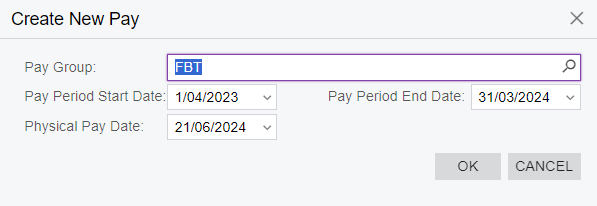

-

Select the new pay group and click OK.

-

Once the pay is OPEN then “View Pay Run”.

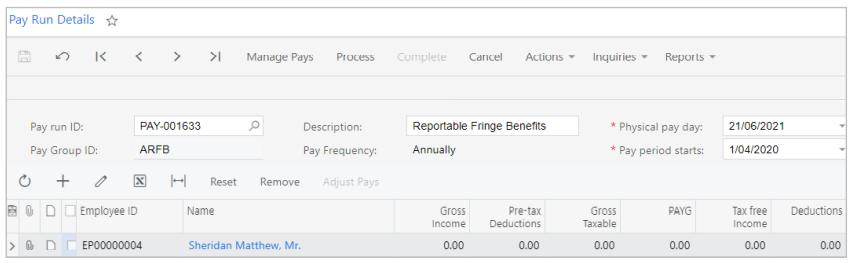

When Single Touch Payroll (STP) is active in MYOB Advanced People, you MUST enter a date for the Physical pay date; no later than 30th June of that financial year. Having a Physical pay date of 31st March would be outside of ATO reporting requirements.

-

Open each employee’s pay and add the Reportable Fringe Benefits (RFB) pay item that matches the reporting requirements of that employee’s fringe benefit.

Send the pay event data to the ATO

-

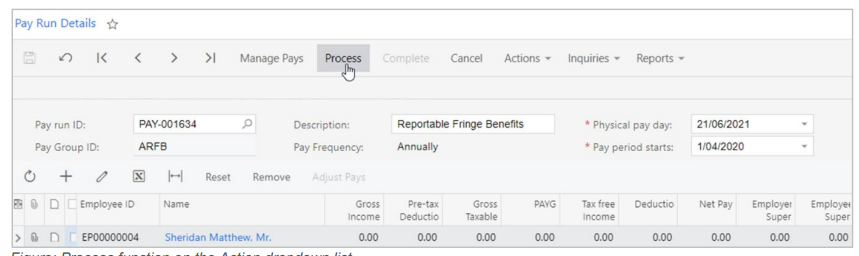

Once all employees have been updated for RFB then return to the pay run by clicking on the Pay Run ID.

-

Process pay run

-

On the Pay Run Details form (MPPP3120) from the main toolbar, select Process.

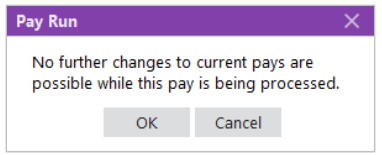

A Pay Run popup will appear.

-

Once you select OK you can only cancel or complete the Pay Run. The Pay Run Status changes to PROCESSING.

-

-

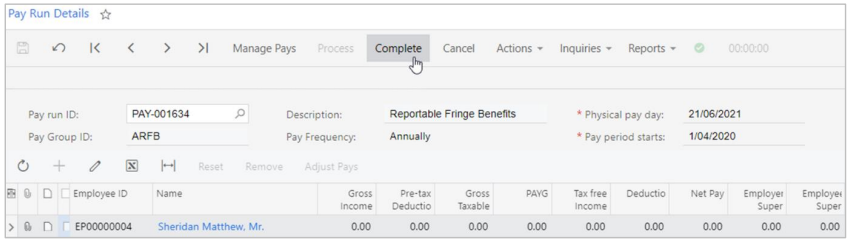

Complete pay run

-

Staying on the Pay Run form, from the main toolbar, select Complete.

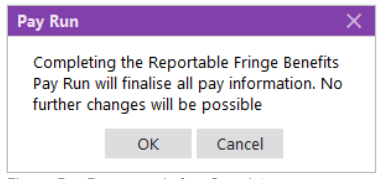

The following Pay Run popup appears:

-

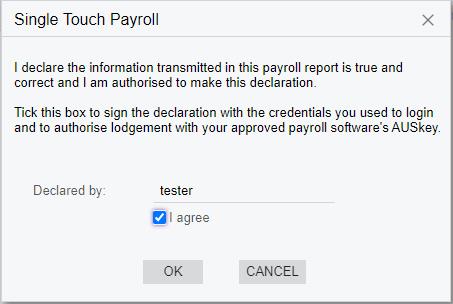

Once you select OK, the pay event declaration will appear

-

Once you tick the checkbox I agree, and then select OK, the pay event declaration will appear. The Pay Run is complete.

-

4. Finalise your STP reporting

The last step for end-of-financial-year procedures is to finalise your STP reporting. On the STP Finalise screen (MPPP5023), you can submit a finalisation event to the ATO. You must send your finalisation event for the current tax year before July 14 2024.

After finalising, your employees can access their information in ATO site to complete their income tax return.

For more information about finalising your STP reporting, see Single Touch Payroll. These pages also cover the changes for STP Phase 2. All customers must use STP Phase 2 unless you have a deferral from the ATO.

If you're an employer with closely held payees, you can find more information on the ATO website.