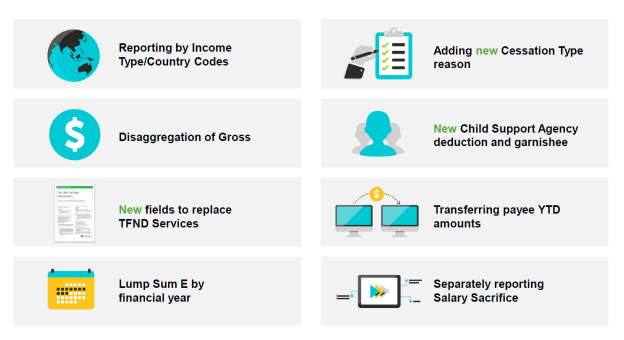

What are the key changes?

Employee reporting changes

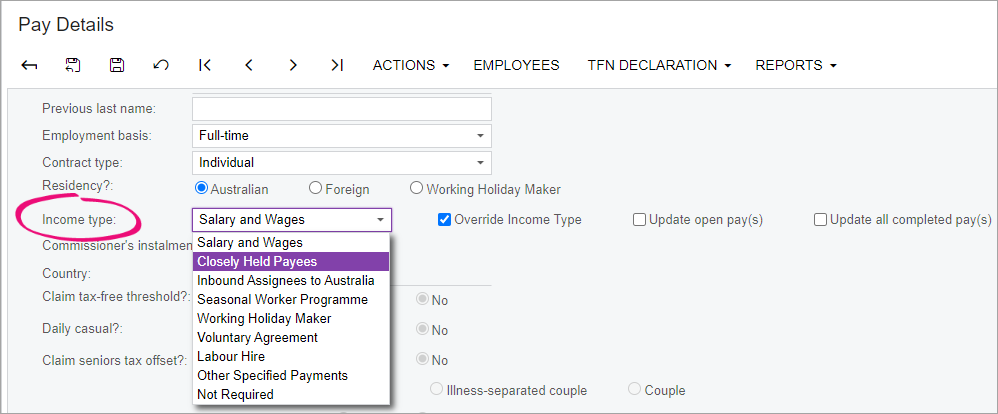

Reporting by income type

In STP Phase 2, the terminology previously known as Payment Summary Type has been replaced with a new term and definition called “Income Type”.

This change has the most impact on those employee’s currently reported as Payment summary type “Individual Non-Business” (INB). The ATO now require this group to be split up into 4 new types.

-

Salary & Waged employees (SAW)

-

Inbound Assignees to Australia (IAA)

-

Closely Held Payees (CHP)

This option is available but, MYOB Acumatica does not have a deferred lodgement capability for-pay events, these are always sent automatically on completion of a pay run. Finalisation events can be processed at the user's discretion.

Seasonal Workers Programme (SWP)

MYOB Acumatica supports this change by:

-

Providing a new screen where you can review all employees. It includes:

-

An action that defaults the likely Income type

-

Ability to review and update remaining employees where the default update action was unable to determine an employee’s Income type

-

An action to apply the reviewed changes to all employee’s current configuration and historical records

-

-

The assigned Income type will be visible on the Taxation tab of the Employee’s pay Detail's record

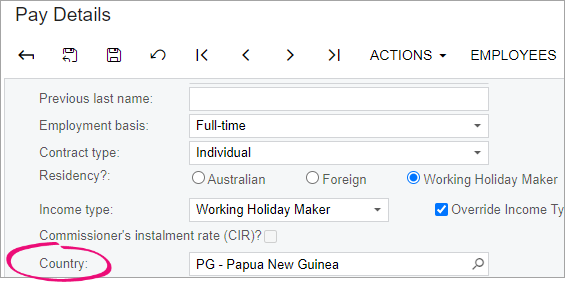

Reporting by country code

Australia has tax treaties with many countries to reduce or eliminate double taxation caused by overlapping tax jurisdictions. Income types must report the YTD income by Country Code to assist Australia to meet its international commitments. However, this only impacts employees classed as “IAA” or “WHM”:

-

IAA employees must report the country they were a tax resident of before coming to Australia

-

WHM employees must report their “home” country

MYOB Acumatica supports the country code you need to capture via a new field called Country, located on the Taxation tab of the Employee’s Pay Detail's record.

Removal of the Onboarding section (or TFN Declaration data)

To replace the former Onboarding section there is now a section in the payload called ‘Employment Conditions’. This section captures more information about the employee and the information sent in this section is sent in every STP event rather than just once. New information captured is the “Employment Basis Codes”, “Tax Treatment Codes” and “Tax offset Amount”. These fields provide context to the changes in the financial amounts for each Pay Event for government agencies using this data. This may allow them to limit the number of contacts with the payer or payee to seek further information about the data submitted.

Employment Basis Codes

The employment basis selection was used to help inform the TFN declaration. In STP phase 2 this field has been expanded with new options and will now report in each STP event.

Existing codes:

-

Full-time – a person who is engaged for the full ordinary hours of work as agreed between the payer and the payee and/or set by an award, registered agreement or other engagement arrangements. A full-time payee has an expectation of continuity of the employment or engagement on either an ongoing or fixed-term basis.

-

Part-time – a person who is engaged for less than the full ordinary hours of work, as agreed between the payer and the payee and/or set by an award, registered agreement or other engagement arrangements. A part-time payee has an expectation of continuity of the employment or engagement on either an ongoing or fixed-term basis.

-

Casual – a person who does not have a firm commitment in advance from a payer about how long they will be employed or engaged, or for the days or hours they will work. A casual payee also does not commit to all work a payer may offer. A casual payee has no expectation of continuity of employment or engagement.

-

Labour Hire – a contractor who has been engaged by a payer to work for their client. The hours of work and duration of engagement are not factors for consideration. This will include contractors who have provided a voluntary agreement with a payer that arranges for persons to perform work or services, or performances, directly for clients of the entity.

Additional codes for Employment basis:

-

Voluntary Agreement – a contractor with their own ABN and is an individual person, rather than a business. The hours of work and duration of engagement are not factors for consideration. This data is unlikely to be sourced from a TFND, as contractors with an ABN are not obliged to provide their payer with a TFND.

-

Death Beneficiary – the recipient of an ETP death beneficiary payment who is either a dependant, non-dependant or trustee of the estate of the deceased payee. This is only to be used if the death beneficiary is not an existing employee on the payroll with a current, valid employment basis.

-

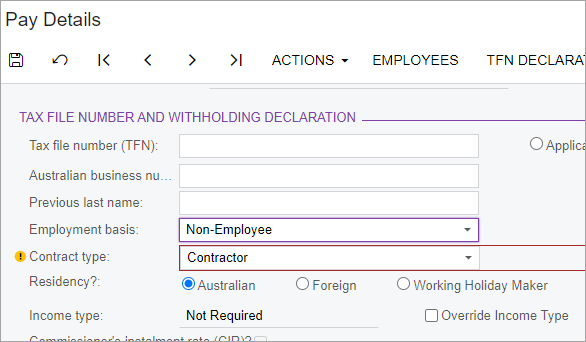

Non-Employee – a payee who is not in the scope of STP for payments but may be voluntarily included in STP for superannuation liability reporting only.

MYOB Acumatica allows selection of these new codes via the Employment basis field and contract type fields in Pay Details/Taxation:

Death Beneficiary is now available as an Employment basis option if the contract type is Individual.

Voluntary Agreement is now available and the default Employment basis option when Contract type is set to Contractor.

For Non-Employee’s set:

-

Contract type to 'Contractor'

-

Employment basis to 'Non-Employee'

-

Income type will be set to 'Not Required'

-

Tax Treatment Code will show as DZXXXX

-

Add an ABN

For those Contractors who are not being reported through STP reporting set:

-

Contract type to 'Contractor'

-

Employment basis to 'Not required'

-

Income type will be set to 'Not Required'

-

Tax Treatment Code will be blank

-

Add an ABN

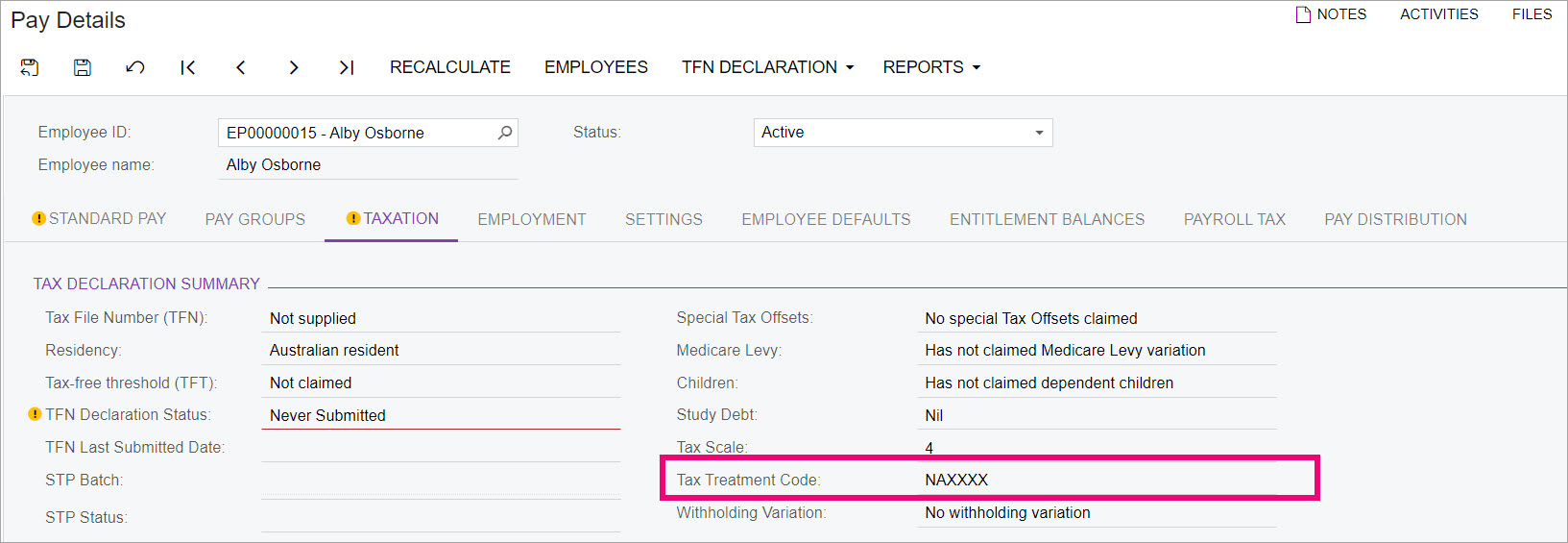

Tax Treatment Codes

Tax Treatment codes help the ATO identify how the employee’s monetary tax values have been calculated.

The Tax Treatment code is a six-character tax treatment code for each employee. The tax treatment code is an abbreviated way of telling the ATO about factors that can influence the amount you withhold from payments to your employees. The ATO has added this code to help:

-

Reduce the need to send TFN declarations to the ATO

-

Help the ATO identify early where an employee has provided incorrect information

MYOB Acumatica will automatically handle the codes to be assigned to each employee. The Tax treatment code can be viewed in an Employees Pay Details taxation screen. When an employees taxation selections are changed the Tax Treatment code will automatically update.

Annual tax offset amount

Not previously reported in STP Phase 1.

Your employee may have given you a Withholding declaration which claims an offset amount to reduce the amount you withhold from their pay. You will need to report the amount claimed in your STP Phase 2 reporting. The annual tax offset amount only applies to regular employees who have claimed the tax-free threshold (meaning you can only report this for employees that you report a tax treatment code beginning in RT).

The ‘Total tax offset’ value is set in the Taxation screen in an Employee’s Pay Details. This value is entered as a yearly total and MYOB Acumatica will calculate the portion to reduce PAYG in each pay, STP reports the ‘Total tax offset’ value.

Cessation reasons

The ATO now collects data that was previously reported to Centrelink via an Employment Separation Certificate. One of the data items the ATO now needs to collect for the Department of Services is a Cessation Reason.

MYOB Acumatica supports the cessation reasons by:

-

Providing a new screen where you can review all employee terminations and add the relevant cessation reasons.

This only needs to be done if you wish to send a new finalisation event for the employee

Adding a cessation reason option in the termination wizard.

Payment reporting changes

MYOB Acumatica supports the following changes for payment reporting by:

-

Providing a new screen where you can review all Pay item’s ATO categories and bulk update pay items

-

An action that defaults the likely Pay item ATO category

-

Ability to review and update remaining pay item categories where the default update action was unable to determine a pay items category

-

An action to apply the reviewed changes to the current configuration and historical records

-

-

Updating the Pay Item liabilities and Pay item types ATO category’s list values

-

System pay items will be updated for new sites and for existing sites via the action to default categories

Not every pay item can be automatically mapped to a valid ATO category. The reason being, the MYOB Acumatica schema does not hold enough information about your pay item records to make business operational decisions that may be unique to your organisation. After upgrading, you are strongly advised to review the settings of all your pay items and adjust as necessary.

Disaggregation of gross

The employee “Gross” amount you report to the ATO has been disaggregated into different income assessment groups with each group reported as separate amounts. The social services agencies require these income assessment groups to administer their programmes.

The amount that was reported as “Gross” for Individual Non-business employees in STP Phase 1, will now in STP Phase 2, exclude payments classified as the following:

-

Paid leave

-

Allowances (extension and rule changes to what was already reported)

-

Overtime

-

Bonuses and commissions

-

Directors' fees

-

Lump-sum W (Return to work payments)

-

Salary sacrifice

There are rules that define what can be included against each income type.

Paid Leave

Paid Leave is required to be reported into different groups. These being:

-

Other paid leave

-

Paid parental leave

-

Workers’ compensation

-

Ancillary and defence leave

-

Cash-out of leave in service

-

Unused leave on termination (paid leave type U)

“Time off in Lieu” (TOIL) items that relate to overtime, must be reported as “Overtime” not “Paid leave”. If you currently use only one pay item for this purpose you will now require two, one in relation OTE hours (this is deemed “Paid leave”) and the other in relation to overtime hours.

Allowance Payments

In STP Phase 1 reporting, some allowances are reported separately, and some were reported as part of gross income.

In STP Phase 2, you now need to report all allowances separately. This impacts most income types, not just expense allowances that may have been deductible on your employee’s individual income tax return.

The allowance payment types you will separately report in STP Phase 2 are:

-

qualification and certification allowances (allowance type QN) (new)

-

8x new other allowance type categories (allowance type OD)

-

ND (Non-deductible)

-

U1 (Uniform)

-

V1 (Private Vehicle)

-

H1 (Home Office)

-

T1 (Transport/Fares)

-

G1 (General)

-

Job Keeper (Keeps the pay item aligned to the existing Job Keeper instructions as per the whitepaper)

-

Use pay item description/Payslip label (This option should not be used unless for exceptional cases)

-

Allowance change details

Please refer to the hyperlinks above for more details to help you determine whether you need to remap your existing allowances and/or create new pay items to support the new rules. Allowances reported in groups 1 – 5 have some new ATO guidelines. If you are unaffected by the new guidelines, the only change is how the data displays in the STP payload. Allowances reported for groups 6 – 8, may have either been reported as an “Other” allowance in STP Phase1 or was included in Gross income.

Don't report:

-

Reimbursements

These are an amount that reimburses an expense that was (or will be) incurred by the employee in the course of their duties and can be verified by receipts some reimbursements may be subject to FBT -

Fringe benefits

These are not amounts that you are paying to your employee. These amounts (if reportable) will continue to be identified using the ATO Reporting Category “Reportable fringe benefit”

Overtime

You will need to review how your organisation has been recording/transacting payments relating to Overtime, which is defined as work done:

-

Beyond their ordinary hours of work

-

Outside the agreed number of hours

-

Outside the spread of ordinary hours (the times of the day ordinary hours can be worked)

For pay items used to make these payments, you will need to check the Include in Super flag is correctly set to “Yes” and the ATO reporting category has been set to “Overtime”.

Special cases to be reported as overtime:

-

TOIL (time off in lieu); only cashed-out amounts are to be reported as overtime. If you have been using one pay item to manage TOIL, you will now require a minimum of 3:

-

TOIL taken

-

TOIL cashed-out

-

TOIL unused leave on termination

-

-

Call back/recall allowances; are overtime when an employee has left the workplace or completed their ordinary time without any prearranged agreement to work overtime but is called back to work overtime.

-

On-call/Stand-by or Availability items; may or may not be classed as overtime. Please check the employee’s Award. For example, if paid as per:

-

clause 31.2 of the MA000036: Plumbing and Fire Sprinklers Award 2010. These types of payments are not ordinary time earnings and should be reported as Payment Type – Overtime

-

clause 20.3 of the MA000031: Medical Practitioners Award 2020. These payments are ordinary time earnings and should be reported as Allowance Type-KN (Task Allowances)

-

-

Leave loading that is demonstrably referable to a notional loss of opportunity to work overtime is not ordinary time earnings and should be reported as Payment Type – Overtime.

-

Commissions & Bonuses

-

Commissions & Bonuses that are wholly referable to overtime hours worked are not ordinary time earnings and should be reported as Payment Type – Overtime

-

Commission referable to ordinary hours worked must be reported as Payment Type – Bonuses and Commissions

-

-

Identifiable Overtime component of Annualised Salary – This will need to be paid as a separate allowance if it is not already.

-

Part-time additional hours that are paid at a penalty or overtime rate, that do not accrue leave entitlements, will need to be paid as a separate allowance if they are not already.

-

Travelling time, travelling time outside of ordinary span of hours will need to be paid as a separate allowance if it is not already.

-

Driving rates/kms the excess of the total ordinary hours per period, if no regard to the terms of the award, or the stipulated overtime rate for piece-rate awards that include hourly driving rates and rates per kilometre, are not ordinary time earnings. These payments will need to be paid as a separate allowance if they are not already.

Directors Fees

Directors’ fees include payments to a director of a company, or to a person who performs the duties of a director of the company. In MYOB Acumatica your pay items will need to be mapped to the ATO reporting category “Director’s fees”

CDEP Amount

CDEP values are no longer reportable, but the STP schema still includes space for it. The monetary value will be zero or blank.

Salary Sacrifice Amount

Not previously reported in STP. In STP Phase 2 you must separately report salary sacrificed amounts.

When reporting salary sacrificed amounts, there are two new types to report:

-

superannuation (salary sacrifice type S) – for superannuation to a complying fund or retirement savings account (RSA)

-

other employee benefits (salary sacrifice type O) – for benefits other than super.

If your employee has an effective salary sacrifice arrangement, you have previously reported post-sacrifice amounts to us. This changes as part of STP Phase 2. You now need to report the salary sacrifice amounts and separately report the pre-sacrificed income amounts in your STP report.

These options have been added to MYOB Acumatica pay item ATO categories “Salary sacrifice super“ and “Salary sacrifice other“. The super option will default in the bulk update pay items action

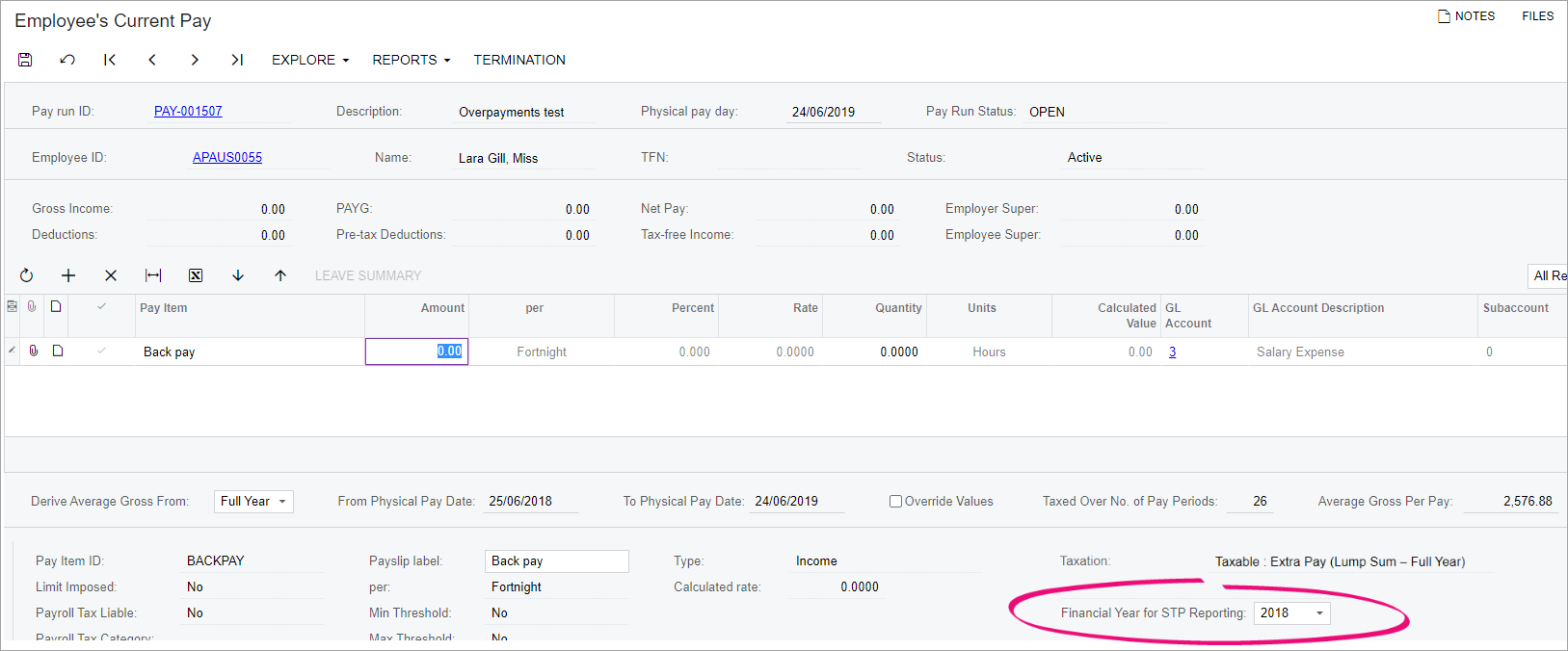

Lump Sum E

Lump sum E is an amount of back payment of remuneration that accrued, or was payable, more than 12 months before the date of payment and is greater than or equal to the Lump sum E threshold amount ($1,200).

You must report Lump sum E YTD amounts by specifying each prior financial year to which the amount relates.

MYOB Acumatica has added the ability to capture the year for Lump sum E payments by:

-

Providing a screen that lists all lump sum E payments, and allows you to select which year the payments relate to

-

Adding a new option in the pay where lump sum E pay items are being processed will capture the FY the payment relates to.

Lump Sum W (return to work)

Not previously reported in STP.

A “Return to Work” amount is paid to induce a person to resume work, for example, to end industrial action or to leave another employer. It does not matter how the payments are described or paid, or by whom they are paid.

These types of payments, to induce workers to return to the workplace, cannot be classified as Payment Type – Bonuses or Commissions or Lump Sum Type-E but must be taxed as “Return to Work” payments (as per NAT3347 Return to Work Payments) and reported as Lump Sum Type-W YTD amounts.

MYOB Acumatica supports this as follows.

-

Return to work for non-working Holiday Makers

-

Pay item with the ATO Category set to “Lump Sum W“

-

Pay item set with Taxation “Taxable : Custom rate“

-

Set Legislated ‘Return to Work’ as true

-

-

Return to work for Working Holiday Makers

-

Pay item with the ATO Category set to “Lump Sum W“

-

Pay item set with Taxation “Taxable : Standard PAYG“

-

Changes for those migrating to MYOB Acumatica

Transferring Payee YTD amounts

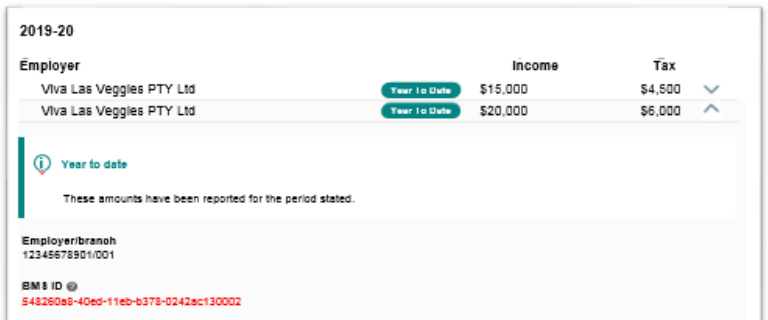

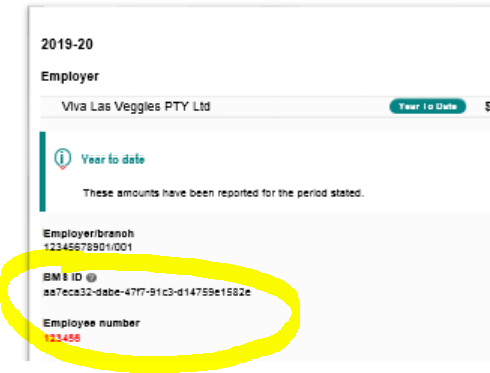

In STP phase 1, payers, changing where your data was stored (software product, Company instance) or changing the employee’s employee code, resulted in an employee having multiple payment summary records with MyGov and YTD values being incorrect.

See ATO reference for “Changing your payroll solution or employees’ Payroll IDs during a financial year”

Example of multiple records for the same employer and employee due to employer changing software:

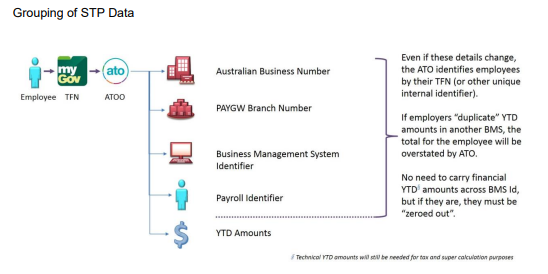

Each unique combination of BMS ID (Unique id for Employer/software) and payroll ID (Employee id in software) the ATO will create a unique income statement record which will be made available in ATO Online accessed through myGov and pre-filled into the IITR. This process is similar to where payers previously would have issued multiple payment summaries to their payee(s).

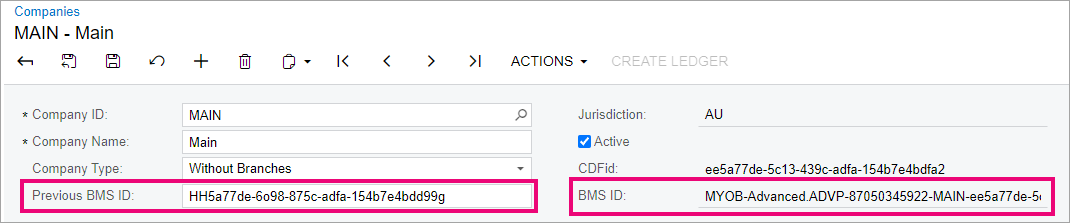

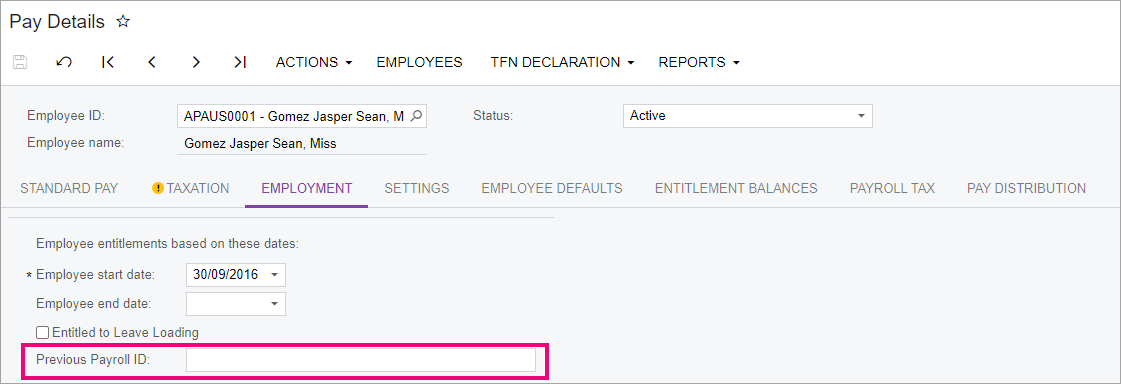

Replacing key identifiers in MYOB Advanced

MYOB Acumatica has added:

-

A new field for Previous BMS ID in Companies. Also, the screen now displays the current BMS ID.

-

A new field for Previous Payroll ID in Employee's Pay Details

-

The previous BMS IDs and Payroll IDs can be found in the previous software used and also in the ATO portal myGov. Also, there are currently no default imports for Pay Details or companies to upload these values on mass, but work is planned for a default import for Pay Details

A new screen to allow you to send a 'once off' update in alignment with the ATO instructions “Previous ID Update - MPPP5027“This screen allows you to:Select the company the employees have been moved toSelect the employees where you need to report their ‘Previous Payroll IDs’ (You can include terminated employees if you have migrated their YTD values using the ‘include inactive’ flag)Review the employee's ‘Previous Payroll IDs’Review the companies 'Previous BMS ID'Submit a ‘once off’ Update STP event to the ATO containing the previous IDS

Simplified batch statuses

Status descriptions for STP submissions have been simplified. There are now only three statuses:

-

Submitted

-

Accepted

-

Failed.